The Securities and Exchange Board of India, vide circular dated November 13, 2020, has introduced a fine and penalty structure for non-compliances with continuous disclosure requirements by issuers of debt instruments.

On January 22, 2020, SEBI issued a uniform structure for imposing fines for non-compliant issuers of listed equity shares. Keeping in view the same, the Capital Market Regulator, in consultation with various market participants, issued the instant circular to ensure effective enforcement of continuous disclosure obligations by issuers of listed debt securities. This circular will be applicable on the following listed instruments:

- Non-Convertible Debt Securities (NCDs);

- Non-Convertible Redeemable Preference Shares (NCRPS); and

- Commercial Papers (CPs)

Effective Date: The fine structure prescribed in this circular will be effective from compliance periods ending on or after December 31, 2020.

The fine structures, as per the above mentioned SEBI circular are as follows:

Part A – Fine to be levied in case of non-compliances by issuers of listed NCDs and/or NCRPS:

|

S. No. |

Regulation |

Non-compliance |

Fine payable and/or other action to be taken for non-compliance |

| (a) |

Reg. 50(1)/(3) |

Delay in furnishing prior intimation with respect to date of payment of interest/ redemption amount or intimation regarding board meeting effecting the rights or interest of holders of NCDs/NCRPS. |

Rs. 1000 per ISIN |

| (b) |

Reg. 52(1) |

Non-submission of the financial results within the period prescribed under this Reg. |

Rs. 5000 per day* |

| (c) |

Reg. 52(4)/ 52(6) |

Non-disclosure of line items prescribed under Regulation 52(4) along with the half yearly/ annual financial results or non-disclosure of items pertaining to NCRPS as notes to financials prescribed under Regulation 52(6). |

Rs. 1000 per day |

| (d) |

Reg. 52(5) |

Non-submission of a Certificate signed by the Debenture Trustee taking note of the contents prescribed under regulation 52(4). |

Rs. 1000 per day |

| (e) |

Reg. 52(7) |

Non-submission of deviations/ variations in utilization of issue proceeds |

Rs. 1000 per day |

| (f) |

Reg. 54(2) |

Non-disclosure of extent and nature of security created and maintained with respect to secured listed NCDs in the financial statements. |

Rs. 1000 per day |

| (g) |

Reg. 57(1) |

Non-disclosure of information related to payment obligations |

Rs. 1000 per day per ISIN |

| (h) |

Reg. 59(1) |

Failure to obtain prior approval of stock exchange for any structural change in terms of NCDs/ NCRPS |

Rs. 50,000 per instance |

| (i) |

Reg. 60(2) |

Delay in submission of the notice of record date |

Rs. 10,000 per ISIN |

| (j) |

Reg. 62 |

Non-compliance with norms pertaining to functional website |

Advisory/warning letter per instance of non-compliance per item Rs. 10,000 per instance for every additional advisory/warning letter exceeding the four advisory/ warning letters in a financial year. |

| (k) |

Chapter III of SEBI (LODR) Regulations, 2015 |

Non-compliance of provisions as stated under Chapter III of SEBI (LODR) Regulations, 2015 (Common Obligations of listed entities) |

Fine payable as per SEBI Circular dated January 22, 2020 |

Part B – Fine to be levied in case of non-compliances by issuers of listed Commercial Papers:

|

S. No. |

Clause |

Fine payable and/or other action to be taken for non-compliance |

| (a) |

Non-submission of financial results within the prescribed period |

Rs. 5000 per day* |

| (b) |

Non-disclosure of line items prescribed under Reg. 52(4) of SEBI LODR Regulations along with the half yearly / annual financial results |

Rs. 1000 per day* |

| (c) |

Non-submission of certificate regarding fulfilment of payment obligations |

Rs. 1000 per day per ISIN |

*Not applicable if the issuer has listed both equity and debt instruments, and penalty in terms of SEBI Circular dated January 22, 2020 for non-compliance of Reg. 33 of SEBI (LODR) Regulations, 2015 has already been levied on such issuer.

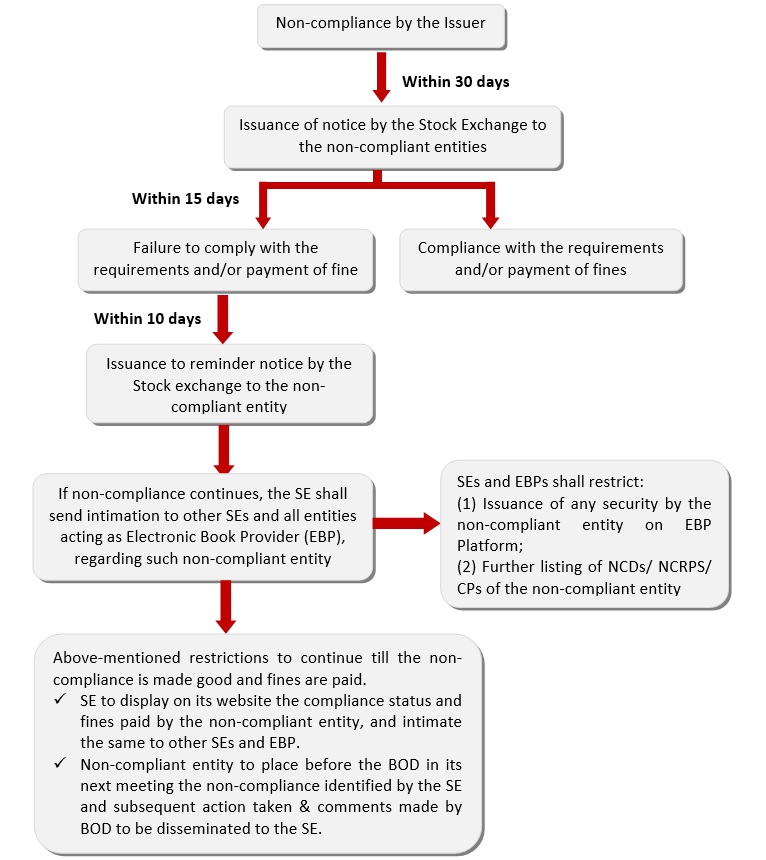

Action to be taken by the Stock Exchanges in case of non-compliance:

CP Remarks:

Since, the promulgation of SEBI Listing Regulations in the year 2015, there was no fine or penalty circular for non compliances in case of listed debt securities. After 5 years, such uniform mechanism has been prescribed. The issuance of said circular will make the companies, whose debt securities are listed, more responsible towards the compliances under the Listing Regulations. Further, in an unfortunate event of any lapse, the companies will be able to settle out their delay/ non compliance by payment of fines and penalties, which otherwise could have acted as impediment in coming with other fund raising capital market transactions by corporates.