Under the RBI Law, FDI and ODI valuations are required to be submitted along with relevant forms for completing FDI/ODI transactions.

Under the Law:

FDI price stands as the Minimum Price and

ODI price stands as the Maximum Price

for any such transaction from an Exchange Control perspective.

All FDI and ODI transactions require proper planning regarding value assessment to avoid any discrepancy in contractual understanding and fair value.

These regulations are put in place to ensure that any Investment going out of the country or coming into the country is done at the Fair Price.

(A) Foreign Direct Investment

- Foreign Direct Investment refers to direct investment equity flows in the reporting economy. It is the sum of equity capital, reinvestment of earnings, and other capital.

- Direct Investment is a category of cross-border investment associated with a resident in one economy having control or a significant degree of influence on the management of an enterprise that is resident in another economy.

- Apart from being a critical driver of economic growth, Foreign Direct Investment (FDI) has been a major non-debt financial resource for the economic development of India.

Case A

Case B

In case of an unlisted Indian company – A SEBI Registered Merchant Banker or a CA

Some reasons for foreign companies to invest in India include:

- Relatively Lower Wages

- Special Investment Privileges

- Increased Growth of Investment

- Provides Tax Incentives

- Boosts Growth and Development Prospects

(B) Overseas Direct Investment

- Overseas Direct Investment or ODI is an investment made outside India in a Joint Venture (JV) or Wholly Owned Subsidiary (WOS) either under Automatic Route or Approval Route.

- The investment is made by contribution to capital, subscription to memorandum of a foreign company, or acquisition of existing shares of a foreign entity by market purchase, private placement or stock exchange.

- Indian person forms a WOS/JV outside India

- Indian person acquires or transfers stake in a foreign entity

The Authorized Dealer (AD) bank shall ensure compliance with arm's length

pricing taking into consideration the valuation as per any internationally accepted pricing methodology for valuation.

The AD bank, as per its recommendation may suggest a Merchant Banker, Registered Valuer or any other professional to calculate the arm's length pricing.

The various benefits of investing overseas include:

- Penetration of Indian Money overseas

- Diversification Benefits

- Advantageous w.r.t Interest and Currency Rate Benefits

- Augment Domestic Investments

- Promote Industrial Development

- Generate Employment

At what Point of Time is Valuation required?

- Valuation done for FDI/ODI transactions is valid for a period of 90 days. Therefore, the transaction should be completed within 90 days from Date of Valuation.

Valuations under Foreign Exchange Management Act

- With the occurrence of more and more FDI transactions in India, the requirement of securities valuation under FEMA will drastically increase. The requirement for such valuations will be triggered at various point of time under various regulatory authorities in India.

- As per RBI guidelines, the Fair Value of Equity Shares, Compulsory Convertible Capital Instruments, or any other Capital Instruments of an Indian Company, in case of allotment or transfer to or from Non-Resident must be carried out in accordance with any internationally accepted valuation methodologies.

- Under the RBI Law, FDI and ODI valuations are required to be submitted along with relevant forms for completing the share transaction. Under the Law, FDI price stands as the Minimum Price and ODI price stands as the Maximum Price for any such transaction from an Exchange Control perspective.

- Valuation is required when the company shares/ debentures are measured based on the fair and actual value received from them. Thus, all FDI and ODI transactions require proper planning regarding value assessment to avoid any discrepancy in contractual understanding and fair value.

The Pricing / Valuation Guidelines are governed by The Foreign Exchange Management Act, 1999 (FEMA), Foreign Exchange Management (Non-Debt Instruments) Regulations, 2019 and RBI notification & regulations issued and updated on time to time.

The final crux of the Pricing/Valuation Guidelines is summarized hereunder:

- Issue by an Indian company or transferred from a resident to non-resident – Price should not be less than

- Listed Company – The price worked out in accordance with the relevant SEBI guidelines

- Unlisted Company – The fair value worked out as per any internationally accepted pricing methodology for valuation on an arm’s length basis, duly certified by a Chartered Accountant or a SEBI registered Merchant Banker or a practicing Cost Accountant.

- Transfer from a non-resident to resident – Price should not be more than

- Listed Company – The price worked out in accordance with the relevant SEBI guidelines

- Unlisted Company – The fair value as per any internationally accepted pricing methodology for valuation on an arm’s length basis, duly certified by a Chartered Accountant or a SEBI registered Merchant Banker.

- Transfer from a non-resident to resident – Price should not be more than

- Listed Company – The price worked out in accordance with the relevant SEBI guidelines.

- Unlisted Company – The fair value as per any internationally accepted pricing methodology for valuation on an arm’s length basis, duly certified by a Chartered Accountant or a SEBI registered Merchant Banker.

- Overseas Direct Investment (ODI) Transactions – The AD bank, as per its recommendation may suggest a Merchant Banker, Registered Valuer or any other professional to calculate arm’s length pricing.

- Swap of Capital Instruments – In case of swap of capital instruments, irrespective of the amount, valuation will have to be made by a Merchant Banker registered with SEBI or an Investment Banker outside India registered with the appropriate regulatory authority in the host country

Source (Pricing Gulidlines): https://thc.nic.in

Q. When is Valuation required?

| FDI Valuation |

ODI Valuation |

|

|

Q. Who can do Valuation for FDI purposes?

|

FDI Valuation |

ODI Valuation |

|

|

Q. At what point of time is Valuation required to be done?

- Valuation done for FDI/ODI transactions is valid for a period of 90 Days. Therefore, the transaction should be completed within 90 Days from Date of Valuation.

As per RBI guidelines the fair value of equity shares, compulsory convertible capital instruments or any other capital instruments of an Indian Company, in case of allotment or transfer to or from Non-Resident must be carried out in accordance with any internationally accepted valuation methodologies.

Q. What are the Valuation Methodologies to be used?

- For Listed Companies

- For Unlisted Companies

The listed companies valuation & pricing methods are driven by the Guidelines issued by SEBI.

The transfer or allotment of equity shares or any other capital instruments are regulated as per Pricing / Valuation Guidelines as mentioned above. The transfer or allotment shall be done at fair value which should be valued as per any internationally accepted pricing methodology.

Internationally accepted pricing methodology mainly implies the Discounted Cash Flow (DCF) Methodology. DCF method for valuation of unlisted companies takes into account the future financial projections, a well research discounting rate, all the macro & micro economy risks and other industry norms. Other methods can also be applied by giving appropriate weights to each such method.

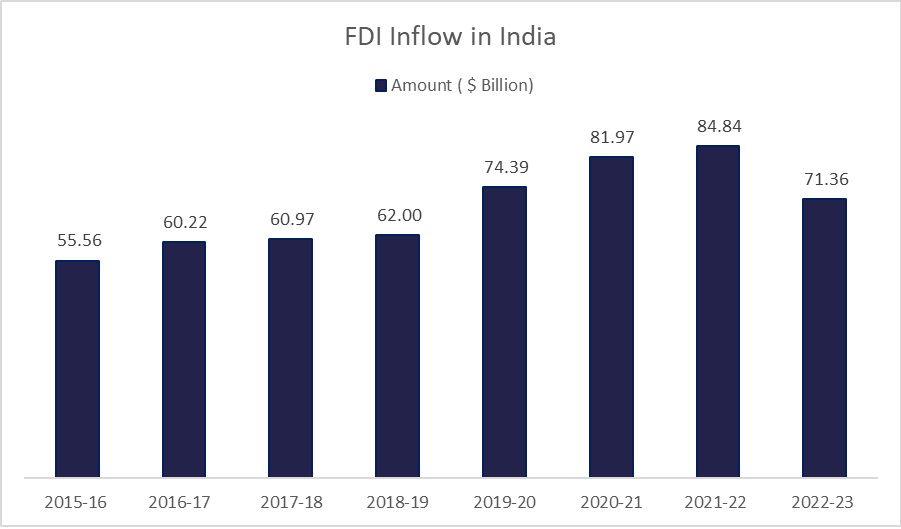

- According to the Department for Promotion of Industry and Internal Trade (DPIIT), FDI equity inflow in India stood at US$ 645.39 billion between April 2000 and June 2023.

- This indicated that the government’s efforts to improve ease of doing business and relaxing FDI norms have yielded results.

- As we can see from the above graph, FDI Inflows in India have increased from $55.56 Billion to $71.36 Billion from 2015-16 to 2022-23. To promote FDI, the Government has put in place an investor-friendly where most sectors are open for 100% FDI under automatic route.

- Further, the policy on FDI is reviewed on an ongoing basis, to ensure that India remains attractive & investor friendly destination. Changes are made after consultation with stakeholders including apex industry chambers, Associations & industry representatives.

- The government has recently undertaken several reforms across sectors. In the last one year alone, reforms in the FDI policy have been undertaken in sectors such as Insurance, Defense, Petroleum & Natural Gas, Telecom, etc.

Future Trends

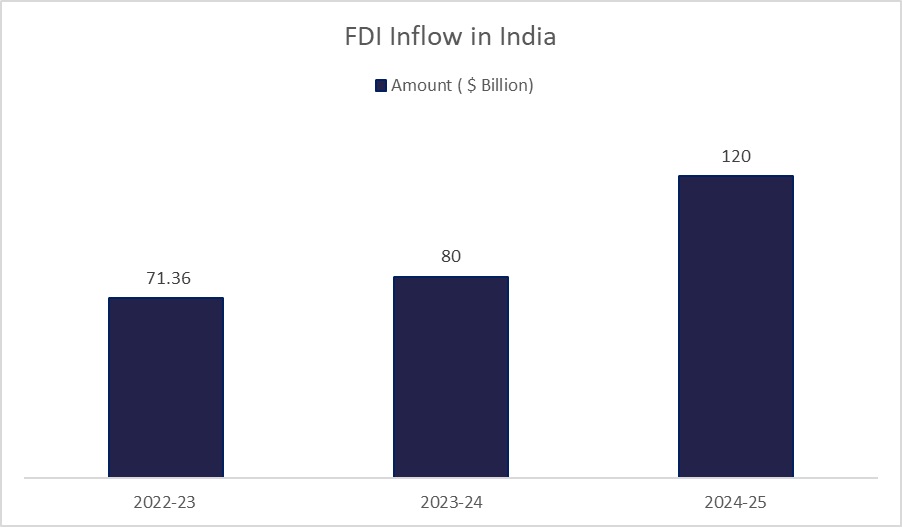

- India is expected to attract foreign direct investments (FDI) of $120-160 Billion per year by 2025, according to a IBEF# report. Over the past 10 years, the country witnessed a 6.8% rise in GDP with FDI increasing to GDP at 1.8%

- In terms of attractiveness, investors ranked India #3; ~80% investors have plans to invest in India in the next 2-3 years, while ~25% reported investments worth >US$ 500 million, the Economic Times reported.

#Source: https://www.ibef.org/economy/foreign-direct-investment

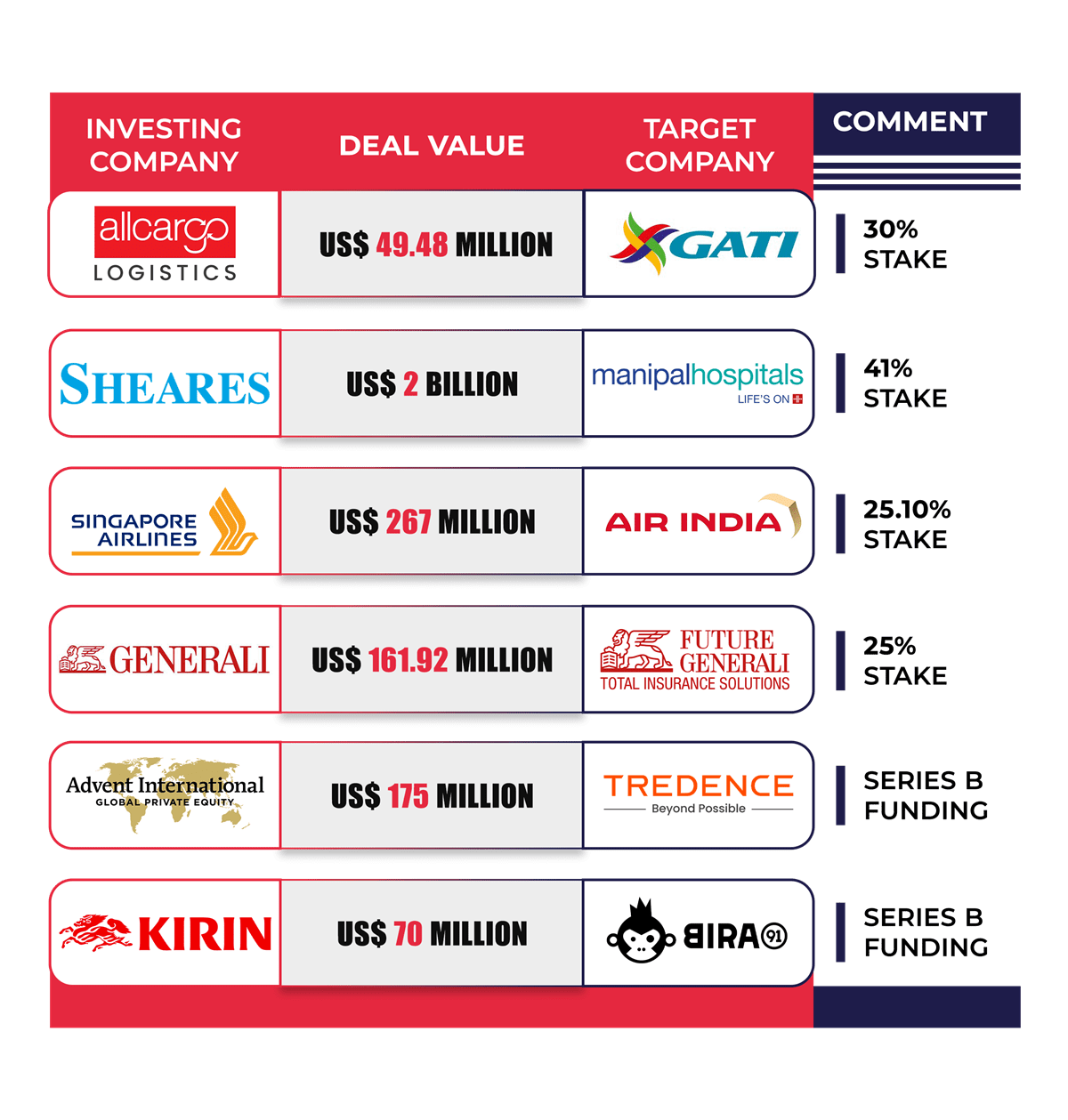

Recent FDI Transactions In India