Overview of Share Valuation

Share valuation plays a pivotal role in corporate finance by determining the fair value of a company’s shares. It provides critical insights for various stakeholders, including investors, shareholders, management, and regulatory authorities. Accurate share valuation facilitates informed decision-making in processes such as:

- Capital Raising,

- Mergers and Acquisitions,

- Employee Stock Options, and

- Financial Reporting

Additionally, it enhances transparency, fosters investor confidence, and ensures fair treatment of shareholders, thereby contributing to the overall efficiency and integrity of financial markets.

Regulatory framework governing Share Issuance Valuation in India

1. Income Tax Act: The Income Tax Act, 1961, is a significant piece of legislation that governs the taxation aspects of share issuance and valuation in India. Under this act, the valuation of shares is crucial for determining the tax implications for both the issuing company and the shareholders. The act provides guidelines for determining the fair market value of shares issued by a company, especially for tax purposes such as capital gains tax, transfer pricing regulations, and tax treatment of share premiums.

2. Foreign Exchange Management Act (FEMA): FEMA, enacted in 1999, regulates foreign exchange transactions in India and oversees cross-border investments. When it comes to share issuance and valuation, FEMA regulations are essential, especially for companies dealing with foreign investors or issuing shares to non-residents. FEMA provisions govern the pricing of shares issued to foreign investors, the repatriation of funds, and compliance requirements for inbound and outbound investments.

3. Securities and Exchange Board of India (SEBI) Regulations: SEBI is the regulatory authority overseeing the securities market in India. While SEBI regulations primarily focus on market integrity, investor protection, and fair practices, they also have implications for share issuance and valuation. SEBI regulations often prescribe disclosure requirements, pricing guidelines, and norms for public offerings, rights issues, and preferential allotments.

4. Companies Act, 2013: The Companies Act, 2013, is another crucial legislation that provides guidelines for share issuance and valuation by companies in India. It outlines provisions related to the issuance of shares, including the types of shares, share capital, share premium, and the process for allotment. The act also mandates compliance with accounting standards for the valuation of shares.

5. Valuation Standards: In addition to specific laws and regulations, there are valuation standards set by professional bodies such as the Institute of Chartered Accountants of India (ICAI) and the Institute of Company Secretaries of India (ICSI). These standards provide guidance on valuation methodologies, principles, and best practices to ensure accuracy and transparency in the valuation process.

Overall, the legal and regulatory framework governing share issuance and valuation in India is multifaceted, encompassing various laws, regulations, and standards aimed at ensuring transparency, fairness, and compliance with tax and foreign exchange regulations. Companies and investors need to navigate these frameworks effectively to ensure compliance and mitigate risks associated with share issuance and valuation activities.

Importance of Share Valuation

Accurate valuation is crucial in determining the fair value of shares for several reasons:

-

- Informed Decision Making: Shareholders, investors, and stakeholders rely on accurate valuations to make informed decisions regarding buying, selling, or holding shares. A precise understanding of a company’s worth helps investors assess the attractiveness of investment opportunities and make strategic decisions aligned with their financial objectives.

- Fairness and Transparency: Accurate valuations promote fairness and transparency in financial markets. They ensure that shareholders are treated equitably and that transactions involving shares are conducted fairly, contributing to market integrity and investor confidence.

- Capital Allocation: Companies use share valuations to allocate capital efficiently. Accurate valuations help management prioritize investment opportunities, allocate resources effectively, and make strategic decisions that maximize shareholder value over the long term.

- Regulatory Compliance: Regulatory authorities often require companies to disclose accurate valuations as part of their financial reporting obligations. Adhering to regulatory standards ensures compliance with applicable laws and regulations, mitigating the risk of legal and regulatory sanctions.

- Mergers and Acquisitions (M&A): Accurate valuations are essential in M&A transactions to determine the fair value of target companies and negotiate favorable terms for shareholders. Precise valuations help acquirers assess the strategic fit, synergies, and potential risks associated with a transaction, facilitating successful deal execution.

In summary, accurate valuation is essential for determining the fair value of shares, promoting fairness and transparency, facilitating informed decision making, and maximizing shareholder wealth. It serves as a cornerstone of effective corporate governance, financial reporting, and capital allocation in today’s dynamic and competitive business environment.

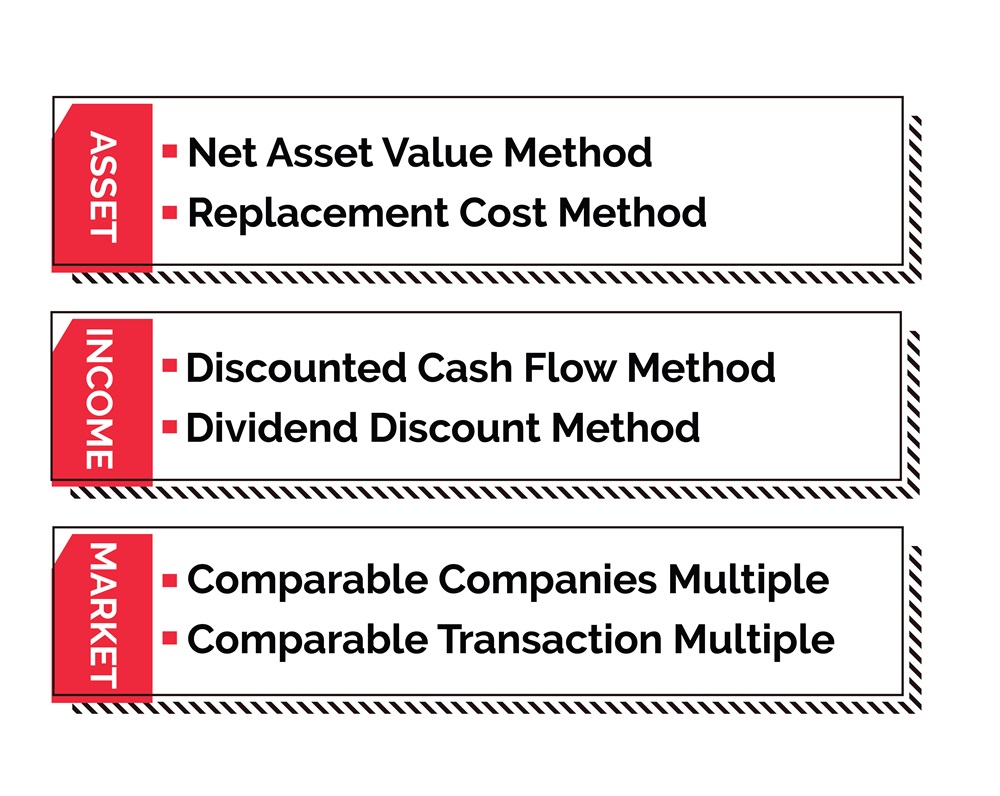

Valuation Approaches and Methods

Share valuation methods encompass a variety of approaches that aim to determine the fair value of a company’s shares. Here is an overview of three primary methods: Market based, Income based, and Asset-based approaches:

1. Market Based Approach:

This approach relies on the principle of market efficiency, using market prices of similar publicly traded companies (comparable) to estimate the value of the subject company’s shares.

Common metrics used in market-based valuation include price to earnings (P/E) ratio, price to book (P/B) ratio, and enterprise value to sales (EV/Sales) ratio.

Comparable companies are selected based on factors such as industry, size, growth prospects, and financial performance, and their valuation multiples are applied to the subject company’s financial metrics to estimate its share value.

| Pros: | Cons: |

| 1. Simplicity and Ease of Use: Market based valuation methods are relatively straightforward and easy to apply, making them accessible for analysts and investors. | 1. Market Volatility: Valuations can be significantly affected by short term market fluctuations and investor sentiment, which may not reflect the company’s long-term value. |

| 2. Reflects Current Market Sentiment: This approach uses current market data, providing a real time snapshot of how similar companies are valued by the market. | 2. Availability of Comparable Companies: Finding truly comparable companies can be challenging, especially for unique or niche businesses. |

| 3. Benchmarking: It offers a useful benchmark by comparing the subject company to its peers, helping to identify over or undervaluation. | 3. Ignoring Internal Factors: This approach may overlook company specific factors such as unique strategic advantages, operational efficiencies, or management quality. |

2. Income Based Approach:

The income-based approach focuses on the future cash flows or earnings potential of the company to determine its share value.

Discounted Cash Flow (DCF) analysis is a commonly used income-based valuation method. It involves forecasting the company’s future cash flows, discounting them back to present value using a discount rate (such as the company’s cost of capital), and deriving the present value of the company’s equity.

Another income-based method is the Dividend Discount Model (DDM), which estimates the present value of future dividends paid to shareholders.

| Pros: | Cons: |

| 1. Focus on Fundamentals: The income-based approach is grounded in the company’s actual financial performance and future cash flow projections, providing a solid basis for valuation. | 1. Complexity and Assumptions: It requires detailed financial projections and assumptions about future performance, which can introduce significant uncertainty and subjectivity. |

| 2. Long Term Perspective: This method emphasizes the company’s future earning potential, aligning with long term investment horizons. | 2. Sensitive to Inputs: Small changes in assumptions, such as discount rates or growth rates, can lead to large variations in valuation outcomes. |

| 3. Flexibility: It can be tailored to account for specific company circumstances and scenarios, offering a detailed and customized valuation. | 3. Data Intensive: This method demands comprehensive financial data and expertise, which can be resource intensive to gather and analyze. |

3. Asset Based Approach:

The asset-based approach assesses the company’s net asset value (NAV) by subtracting its total liabilities from the value of its assets.

This approach is particularly useful for companies with significant tangible assets, such as real estate or manufacturing companies.

There are two variations of the asset-based approach: the going concern approach, which values the company as a continuing business, and the liquidation approach, which values the company based on the sale of its assets in a liquidation scenario.

| Pros: | Cons: |

| 1. Tangible Value: It focuses on the company’s actual tangible assets, providing a clear and concrete basis for valuation. | 1. Ignores Intangible Assets: This method may undervalue companies with significant intangible assets such as brand value, intellectual property, or human capital. |

| 2. Useful for Asset Heavy Companies: This method is particularly suitable for companies with significant tangible assets, such as real estate or manufacturing firms. | 2. Not Reflective of Earnings Potential: It does not consider the company’s future earning potential or cash flow generation capabilities. |

| 3. Simplicity: The asset-based approach can be simpler to apply compared to income-based methods, particularly for asset rich companies. | 3. Static Valuation: The asset-based approach provides a static snapshot of value, which may not capture the dynamic nature of business operations and growth prospects. |

Each of these valuation methods has its strengths and limitations, and the choice of method depends on factors such as the nature of the business, availability of data, and the purpose of the valuation. By considering multiple approaches and triangulating the results, analysts can arrive at a more robust estimate of the fair value of a company’s shares.

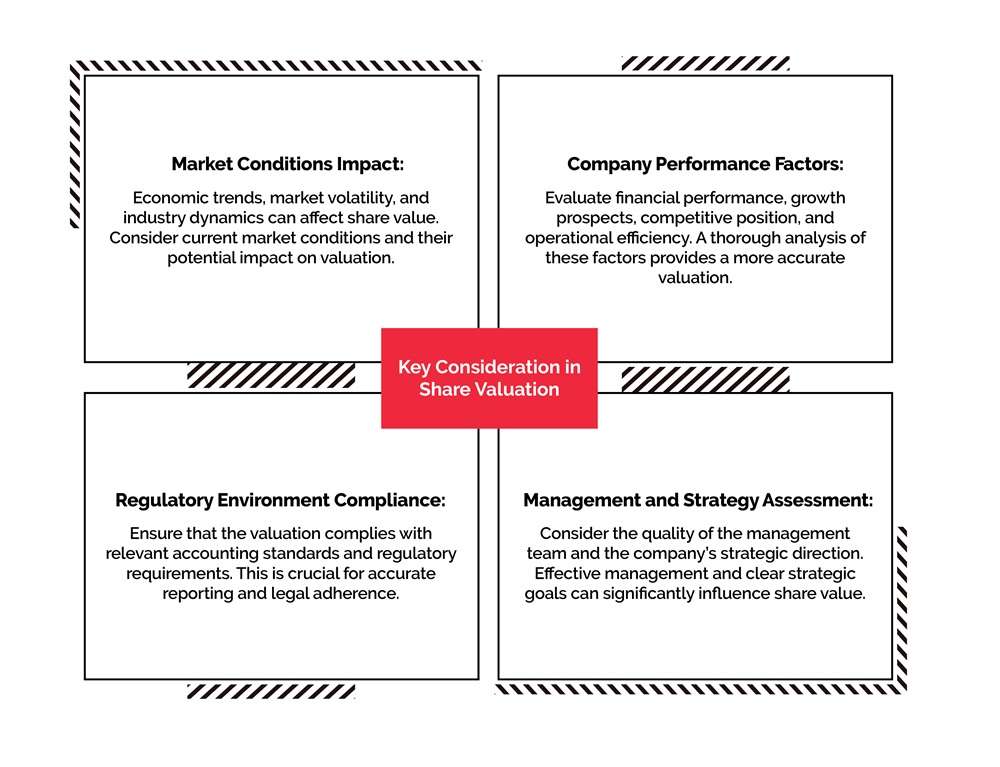

Key Considerations in Share Valuation

Case Studies

Case Study 1: Zomato’s High Valuation Dilemma

Challenge:

Zomato, one of India’s leading food delivery platforms, faced scrutiny over its high valuation leading up to its IPO in 2021. Investors were concerned about the company’s significant losses and minimal profits, which raised questions about its high price-to-earnings (P/E) ratio. Traditional valuation methods indicated that Zomato’s stock might be overvalued, leaving many investors uncertain about the company’s financial health.

Solution:

To address these concerns, investors turned to forward-looking models like the Discounted Cash Flow (DCF) method, focusing on Zomato’s growth potential rather than its current earnings. They analyzed future revenue streams from food delivery, dining services, and strategic partnerships, recognizing the opportunity presented by India’s rapidly expanding digital economy and the increasing demand for convenience services.

Outcome:

Despite initial fluctuations post-IPO, Zomato’s stock valuation has remained strong, supported by investor confidence in its long-term growth trajectory. The company’s ongoing investments in technology and service expansion demonstrate its commitment to capturing market share in a competitive landscape. Zomato’s experience highlights the significance of growth potential in share valuation, emphasizing the need for a forward-looking approach in assessing startups in emerging sectors.

Case Study 2: Jet Airways’ Downfall

Challenge:

Jet Airways, once a major player in India’s aviation sector, faced a dramatic decline that culminated in its grounding in 2019. Investors had previously relied on traditional valuation metrics like the Price-to-Earnings (P/E) and Price-to-Book (P/B) ratios, believing that Jet Airways was undervalued compared to its competitors. However, the airline struggled with mounting debts, high operational costs, and fierce competition, which led to significant financial losses.

Solution:

As the situation worsened, investors who reassessed their analysis began focusing on Jet Airways’ deteriorating cash flow, declining market share, and operational inefficiencies. They realized that the airline’s stock was not undervalued but rather accurately priced, reflecting its ongoing financial challenges. By prioritizing fundamental indicators over traditional metrics, these investors recognized the risks and potential for further losses, leading some to divest before the company’s collapse.

Outcome:

Jet Airways’ stock has remained significantly below its former highs, illustrating that reliance on conventional valuation metrics without a thorough examination of broader financial health can lead to misguided investment decisions. This case underscores the importance of employing multiple valuation methods and considering a company’s overall financial condition when evaluating stock value, particularly in volatile industries like aviation.

Conclusion

The article highlights the crucial role of share valuation in capital-related decisions, mergers, acquisitions, and financial reporting. In India, regulatory frameworks ensure that valuations are conducted fairly and transparently. Key valuation methods include market-based, income-based, and asset-based approaches, each essential for informed decision-making and regulatory compliance. These approaches consider various factors such as company performance, industry trends, and prevailing market conditions.

For effective valuation, best practices involve using comprehensive models, ensuring data accuracy, and adhering strictly to regulatory requirements. This helps companies make well-informed financial decisions while maintaining transparency. Additionally, continuous improvement of valuation models is critical, enabling businesses to adapt to changing market dynamics and regulatory updates. Ultimately, robust share valuation practices drive better financial management and support sustainable growth, ensuring stakeholders’ interests are safeguarded in both domestic and global markets.