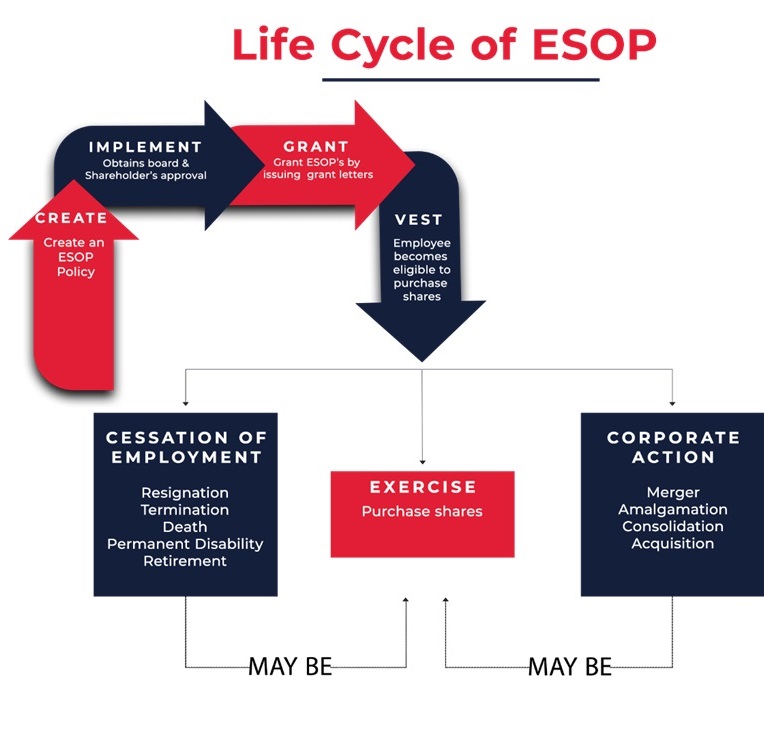

What is ESOP?

An Employee Stock Option Plan (ESOP) or Employee Stock Option Scheme (ESOS) is a program offered by a company to its employees, granting them the option or right to buy the company’s shares at a predetermined price in the future. It’s important to note that ESOP is a voluntary opportunity, not an obligation, allowing employees to acquire a specific number of company shares at a predetermined price of their choice.

Sec 2(37) of Companies Act, 2013 defines “employees stock option” which means, ‘the option given to the directors, officers or employees of the company or of its holding company or subsidiary company or companies, if any, which gives such directors, officers or employees, the benefit or right to purchase, or to subscribe for, the shares of the company at a future date at a pre-determined price.’

6 Different Types of ESOPs – Employee Stock Ownership Plans

- Employee Stock Option Scheme (ESOS): This is the most prevalent type of ESOP. ESOS offers employees the opportunity to buy company shares at a predetermined price, often lower than the market value. These options are typically granted as part of compensation packages and are subject to specific performance criteria over a defined vesting period.

- Employee Stock Purchase Plan (ESPP): ESPP allows employees to buy company stock at a reduced price, enabling them to gradually increase their ownership in the company through periodic investments. ESPP also provides participation in company profits, including dividends.

- Restricted Stock Units (RSUs): RSUs are a form of ESOP that allows employees to convert them into actual company stocks after a specified number of years with the company or upon achieving specific performance milestones. It’s worth noting that RSUs do not come with voting rights or dividends until the vesting period is complete.

- Restricted Stock Award (RSA): RSAs represent a stock-based compensation method where a fixed number of shares is granted to employees, subject to certain restrictions. These restrictions typically depend on the vesting period and other performance criteria. A key distinction from RSUs is that employees do not receive actual shares until the units vest and restrictions are lifted.

- Stock Appreciation Rights (SARs): SARs are an ESOP variant that allows employees to receive payments based on the appreciation of the company’s stock over a specific period. SARs enable companies to provide employees with stock benefits without diluting equity, while employees can benefit from equity gains without exposure to downside risks.

- Phantom Equity Plan (PEP): Phantom Equity Plans closely resemble Stock Appreciation Rights Plans. In a Phantom Equity Plan, employees receive payments based on the company’s stock value without actual ownership of shares. In other words, employees do not receive physical stock certificates but rather receive financial compensation based on the company’s stock appreciation.

Important Terms

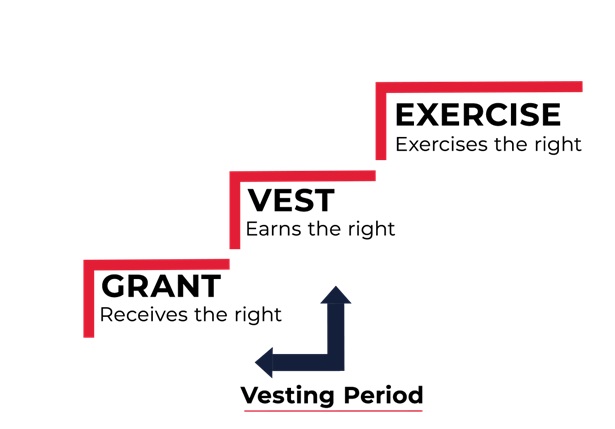

Option: An option represents the right, but not the obligation, to purchase a company’s shares upon meeting the conditions outlined in the ESOP plan. The purchase price is determined at the time of option grant.

Grant: Grant refers to the process of selecting specific employees, typically based on their roles and performance, to receive stock options. It is the act of offering stock options to eligible employees.

Vesting: Vesting indicates an employee’s entitlement to exercise their stock options. Before they can convert these options into actual shares, they must wait for a defined period, as stipulated in the ESOP grant terms.

Exercise: Exercise is the action of converting the stock options awarded to an employee into company shares. This is accomplished by paying the required exercise price, which may be determined by the company within the bounds of applicable accounting policies, if any. The effective date of exercise is when the company formally assigns the shares.

What is ESOP Valuation?

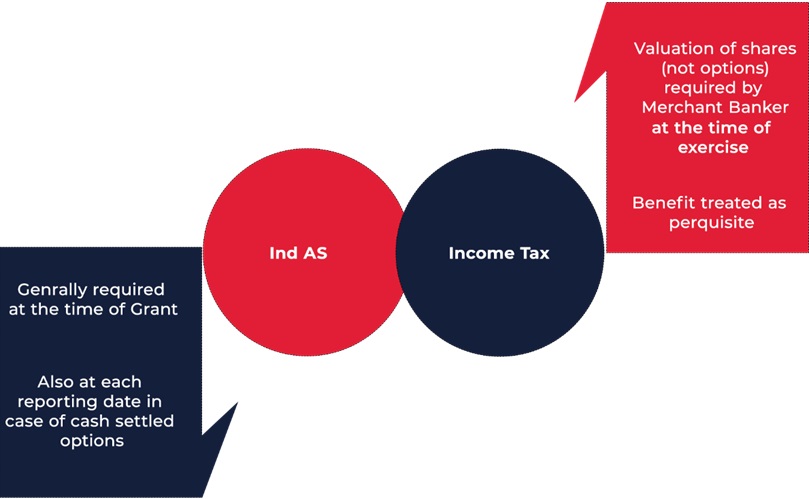

During the grant of options, the fair value of shares is determined by a registered valuer. When employees decide to exercise their options and convert them into actual shares, the valuation is typically conducted by a Merchant banker. This two-step process ensures that the fair value of the shares is properly assessed both when the options are initially granted and when they are exercised, helping to determine the value of the shares at those particular points in time.

Valuation of ESOP in case of Unlisted Companies: The determination of the fair value of shares during the “grant of Option” and “exercise of option” must be carried out by an independent valuer in accordance with the “Guidance note on accounting for employee share-based payment” issued in 2005. While the Income Tax Act of 1961 does not prescribe a specific methodology for calculating the fair market value (FMV) of shares, Section 17 and Rule 3(8) of the Act specify that, to assess perquisites, the FMV of Employee Stock Option Plans (ESOPs) should be based on the value determined by a merchant banker on a specific date.

The term “Specified Date” refers to either the date of exercising the option or any date preceding the exercise date, provided that it is not more than 180 days prior to the exercise date.

When is ESOP Valuation required?

Legal Provisions regarding ESOP Valuation

-

- Valuation Requirement under Ind AS 102- Share Based Payments:

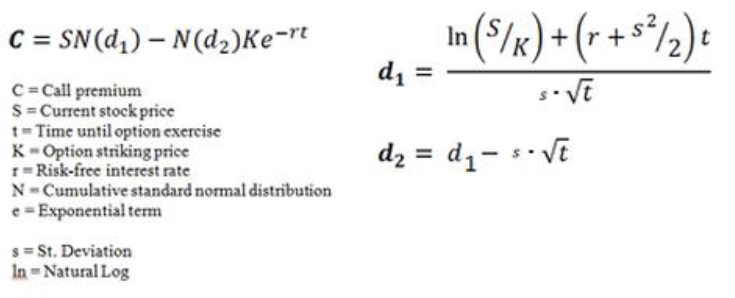

The fair value to be used is not solely based on the quoted price of a security. It takes into account various market-related conditions and non-vesting conditions. Therefore, in determining this fair value, valuation techniques must be employed. However, the Standard does not provide specific provisions for this purpose. Generally accepted and widely used valuation techniques like the Black-Scholes pricing model and Binomial pricing model are commonly utilized to determine the fair value in such cases.

Standard specifies the following minimum inputs to be used while calculating the fair value.

(a) Exercise price of the option;

(b) Life of the option;

(c) Current price of the underlying shares;

(d) Expected volatility of the share price;

(e) Dividend expected on the shares (if appropriate); and

(f) Risk-free interest rate for the life of the option.

Methods Recommended:

-

-

- Black-Scholes: Developed by economists Fischer Black, Myron Scholes, and Robert Merton, the Black-Scholes pricing model is the most renowned and widely recognized option pricing model.

-

Key assumptions of the model:

-

-

-

- The model is designed for European-style options, which means these options can only be exercised at the expiration date.

- The model assumes that stock prices exhibit the log-normal property, implying that the percentage changes in stock prices are normally distributed. This assumption plays a fundamental role in the model’s calculations.

- In its original form, the Black-Scholes model did not factor in equity dividends. However, subsequent refinements to the model have been made to incorporate the impact of dividends on option pricing.

-

-

-

-

- Binomial: More flexible than Black-Scholes-Merton.

-

Key assumptions of the model:

-

-

-

- The model is specifically designed for American-style options, which can be exercised at any time leading up to the option’s expiration date.

- It assumes that stock prices follow a binomial distribution. This means that, over discrete time intervals, the stock price can move in two possible directions, either up or down.

- At each time step, the stock price can move in two directions, leading to two different possible outcomes.

- The model involves creating a tree-like structure with multiple nodes, each representing a specific time interval. This tree helps visualize the potential stock price movements over time.

- At each node, the model calculates the expected share price and the expected option value. This calculation process continues throughout the tree until reaching the final nodes, ultimately providing the option’s estimated value.

-

- Mandatory Valuation Exercise

-

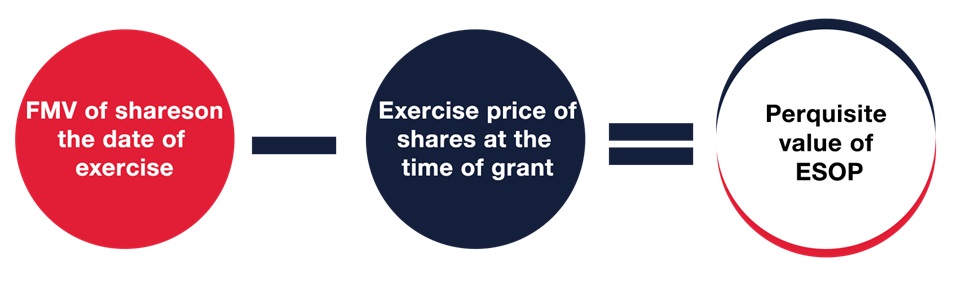

The Income-tax Act, 1961 provides for taxation of ESOPs as a perquisite at the time of exercise, subject to the valuation of the perquisite as prescribed in the Income-tax Rules, 1962.

As per the IT rules, the taxable value of the ESOP on exercise is Fair Market Value (FMV) of the share on the date of allotment / transfer of shares – Exercise Price paid by the employee.

An unlisted company must obtain a valuation certificate from a Category 1 Merchant Banker registered with SEBI as of a date not earlier than 180 days prior to date of exercise.

Fair Value of Underlying, especially in the case of unlisted equity shares based on generally accepted methods like market multiples, DCF etc. We also need to adjust the value via Discount for Lack of Control (DLOC), such that the value arrived at is at minority level and not control level.

As far as Financial Reporting is concerned, for listed companies, there is no specification other than the valuation methodology; however, as it impacts the financial statements, auditors prefer valuations being carried out by trusted and efficient valuers with decent track records.

Tax Implications

-

- For the Employee: When options are granted and as they vest with the employee, there are typically no immediate cash outflows or taxation implications. However, the Income Tax Act, 1961, outlines two stages of taxation for employees in relation to shares allocated to them through an Employee Stock Option Plan (ESOP).

Stage 1 (Perquisites)– When shares are allotted to an employee after they exercise their option upon completing the vesting period, the employer is responsible for calculating the perquisite value of the ESOP. This perquisite value is taxable in the hands of the employee as part of their “income from salary.” The employer is also required to deduct the applicable tax on this ESOP perquisite amount before disbursing it to the employee.

Stage 2 (Capital Gains)–

-

- For the Company:

ESOP costs are deductible expenses for the issuing company. The discounts provided through ESOPs are considered employee costs and can be deducted over the vesting period.

In the case of ESOP share buybacks by an unlisted company, specific sections of the Income Tax Act come into play:

-

-

- Section 10(34A) exempts shareholders from tax on income from such buybacks.

- Section 115QA requires the unlisted company to pay a 20% tax on the buyback.

-

If an employee chooses to sell ESOP shares to a third party, any capital gains tax liabilities arising from the sale are the responsibility of the employee, and the company is not liable for taxes in this transaction.

Amendments introduced vide Budget 2020 for Startups

Finding buyers for startup shares can be challenging due to the absence of an active ESOP market. However, the Income Tax Act provides certain tax benefits for “eligible startups.” Beginning from the fiscal year 2020-21, no tax is payable when employees exercise their ESOP options.

The Tax Deducted at Source (TDS) on the “perquisite” of ESOPs is deferred until one of the following events occurs:

-

-

- 5 years from the ESOP allotment date.

- The date when the employee sells their ESOP shares.

- The date of employment termination.

-

When employees sell ESOP-acquired shares, they are subject to a second tax, similar to capital gains tax, with the tax rate determined by the holding period (short-term or long-term). The cost of the ESOP is considered to be the fair value at the date of exercise, as tax was already paid when the options were exercised.

Guidance Note to ESOP

All option pricing models take into account, as a minimum, the following factors:

(a) the exercise price of the option;

(b) the life of the option;

(c) the current price of the underlying shares;

(d) the expected volatility of the share price;

(e) the dividends expected on the shares (if appropriate); and

(f) the risk-free interest rate for the life of the option

- Life: In the case where early exercise is anticipated, this can be integrated into the duration parameter applied within the option pricing model. It is advisable to examine the historical average duration of actual exercises.

Employees with similar projected exercise behavior can be grouped, and a weighted average duration can be computed for the entire group of employees. - Exercise Price: The exercise price is the amount that the counterparty must pay to exercise the option granted to them as part of the share-based payment arrangement.

- Volatility: It represents the degree of price fluctuations, whether it’s how much a price has fluctuated (historical volatility) or how much it’s anticipated to fluctuate (expected volatility) over a given timeframe. When we talk about the volatility of a stock price, it’s essentially a measure of the standard deviation in the continuously compounded rates of return on that stock over a specific period.

- Dividends: In general, when making assumptions about expected dividends, it’s advisable to rely on publicly accessible information. For a company that neither pays dividends nor intends to do so, it’s reasonable to assume an expected dividend yield of zero. However, emerging enterprises without a track record of dividend payments might anticipate starting to pay dividends within the expected duration of their employee stock options. In such cases, these companies could consider an average that combines their historical dividend yield (typically zero) with the average dividend yield of a relevant and comparable peer group.

- Risk-Free Interest: Usually, the risk-free interest rate is determined by the implied yield offered by zero-coupon government bonds. This yield corresponds to bonds with a maturity period matching the expected duration of the option being evaluated. This expectation takes into account both the remaining contractual term of the option and any considerations related to anticipated early exercise.