Introduction

The Non-Banking Financial Companies (NBFC) are facing increased regulatory and financial pressure amid market volatility. Challenges such as rising risk weights imposed on bank funding in November 2023, higher delinquency rates, and poor recovery rates, particularly in the microfinance sector, are compounding the sector’s struggles. Adding to the woes, smaller NBFCs must now meet the revised Net Owned Fund (NOF) threshold—from Rs. 2 crores to Rs. 5 crores for NBFC-ICC and Rs. 7 crores for NBFC-MFI—by March 31, 2025.

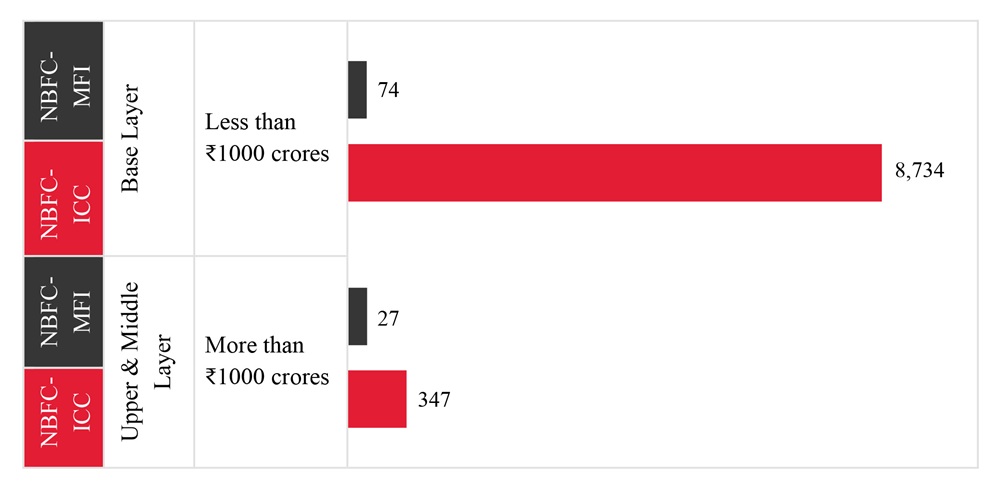

Here, it is pertinent to review the categories of the NBFCs registered with Reserve Bank of India (‘RBI’) and as per the list available on RBI’s website dated October 10, 2024, there are 9,306 NBFCs spanning into different layers i.e. Upper, Middle and Base layer. Considering the asset size of Upper and Middle Layer NBFCs being more than Rs. 1000 crores, their existing NOF is at comfortable position and are already in excess of the new limit of Rs. 5 or Rs. 7 crores. As per RBI data, Upper- and Middle-layer aggregates to 347 NBFC-ICC and 27 NBFC-MFI which represent only 4.50% of all registered NBFCs whereas base layer, whose asset size is less than Rs. 1000 crores, comprises 8,734 NBFC-ICC and 74 NBFC-MFIs which represents 94.64% of all registered NBFCs. There is no publicly available data either on RBI website or any association of NBFCs that can tell us the exact number of the NBFCs whose NOF is lower than Rs. 5 crores and Rs. 7 crores. However, it is clear that under base layer there are smaller NBFCs and many of them do not have required NOF. Considering the smaller asset size and limited resources, these base layer NBFCs would struggle to meet the new limit of NOF before March 31 2025.

Is This a New Challenge for NBFCs?

This regulatory requirement is not an unprecedented event. In 1999, the Reserve Bank of India (RBI) introduced a phased NOF requirement increase for existing NBFCs:

- NOF to be ₹1 crore by March 31, 2016

- NOF to be ₹2 crores by March 31, 2017

A similar pattern is now being repeated, emphasizing RBI’s continued commitment to strengthening the financial stability of NBFCs and ensuring only well-capitalized players remain operational.

What Are the Options Available to Augment Capital?

For NBFCs struggling to meet the NOF threshold, the following strategies may help:

1. Capital Infusion

NBFCs can strengthen their capital base by:

- Raising funds through equity investments from external investors,

- Offering additional shares to existing shareholders, and

- Retaining a larger portion of their profits instead of distributing dividends.

These measures can help NBFCs enhance their financial strength while reassessing their investment strategies to optimize asset returns. Here, it is pertinent to note while raising funds that any change in shareholding beyond 26% whether in single transaction or aggregate thereof, or where there is change in control, NBFC is required to obtain prior approval of RBI before effecting any change in shareholding or control.

2. Mergers and Acquisitions

Mergers and acquisitions (M&A) can be a strategic solution for smaller, undercapitalized NBFCs. By consolidating with financially stronger counterparts or merging with other smaller NBFCs, they can ensure compliance with RBI norms while efficiently utilizing resources. M&A activity can also help avoid regulatory penalties or license cancellations.

3. Conversion into a Core Investment Company (CIC)

There may be some NBFCs which are registered as NBFCs however carrying CIC activities i.e., mainly holding investment in group companies. Thus, such NBFCs need to analyse its structure, holding, its resources before thinking of conversion into CIC. Here, it is also pertinent to note that there are two type of CIC first is ‘Registered CIC’ and other one is ‘Unregistered CIC’. Registered CIC means such financial institution which satisfies both conditions (a) Asset size of more than Rs. 100 crores and (b) raised public funds whereas Unregistered CIC means such financial institutions which does not fulfil either of the conditions.

Moreover, Registered CIC is categorized as one of the forms of NBFCs that fall under the middle layer as per Scale Based Regulations issued by RBI, and thus, it is also required to comply with NOF, including the new limits. While Unregistered CIC is neither required to be registered with RBI nor required to follow NOF norms. Thus, NBFCs that are not in a position to comply with the new limit before the end of this march, may look for this route to convert itself into Unregistered CIC by surrendering their licence.

What Are the Consequences of Failing to Meet the NOF Requirement?

1. Deemed Cancellation of NBFC License

Under RBI’s Scale-Based Regulations, any NBFC failing to meet the revised NOF threshold will automatically lose its Certificate of Registration (CoR) after March 31, 2025.

However, it is not clear whether RBI would provide another chance to meet the higher NOF while releasing a list of NBFCs whose registration has been cancelled on account of failure to achieve new NOF. As discussed at the beginning, such a step was also taken by RBI in the past in 1999 and the last date to achieve the revised NOF limit was March 31, 2017. Post such date, RBI took steps to cancel the licenses of many NBFCs in the financial year 2017-18 and continued to cancel throughout 2018. As per the media reports of that time period, majority of the licences belong to NBFCs whose licenses were cancelled by RBI due to non-adherence of revised NOF criteria and in fact, some NBFCs had surrendered their certificates of registration due to failure to achieve that revised limit.

2. Ban on Onboarding New Customers

NBFCs that fail to meet the NOF threshold will be barred from conducting new financial activities. While they may continue servicing existing customers, but they cannot disburse fresh loans even if that is as per a pre-existing obligation. However, in the interest of customer and financial system, they must still adhere to existing RBI norms, including:

- Know Your Customer (KYC) compliance

- Reporting to Credit Information Companies (CICs)

- Maintaining loan provisioning norms

Consequences of CoR Cancellation: Ongoing Obligations for NBFCs

A recent RBI circular dated October 10, 2024, though it was concerning credit reporting, clarifies that institutions/ NBFCs whose CoR has been cancelled must continue reporting credit information for all borrowers onboarded before cancellation.

- This reporting obligation continues until either the loan tenure ends or the NBFC is wound up, whichever occurs first.

- Cancelled NBFCs will still have access to borrower credit reports via CICs for accounts reported before cancellation.

Is There Any Remedy for Affected NBFCs?

Can NBFCs legally challenge the RBI’s NOF requirement? The answer is no.

Under Section 45-IA of the RBI Act, 1934, the Central Bank has the absolute authority to prescribe NOF limits and notify the revised limits from time to time. However, before cancelling any license under any ground including failure to meet NOF requirements, RBI is required to offer a reasonable opportunity to affected NBFCs.

NBFCs that cannot meet the NOF requirement by March 31, 2025, may consider:

- Submitting an application to RBI with a detailed action plan explaining how and when they will meet the NOF threshold. If found valid, RBI may grant an extension.

- If RBI rejects the request and proceeds with cancellation, the NBFC can file an appeal within 30 days before the Tribunal set up by the Ministry of Finance, whose decision will be final and binding.

Conclusion

The revised NOF requirement for NBFCs is a significant regulatory shift aimed at strengthening the sector. While Upper and Middle Layer NBFCs are well-positioned to comply, smaller Base Layer NBFCs face severe challenges in raising capital within the given timeline.

The regulatory approach mirrors previous measures taken by RBI in 1999 and 2017, signalling its continued intent to consolidate and professionalize the NBFC landscape.

For NBFCs at risk, capital infusion, M&A activity, or conversion into CICs may be viable solutions. However, failure to comply will result in license cancellation, operational restrictions, and ongoing reporting obligations.

To mitigate the risk of losing their licenses, NBFCs must proactively assess their financial standing, engage with investors, explore restructuring options, and communicate with RBI for possible extensions.