Amid COVID-19 crisis impact, many cash-rich companies are coming out for shopping with buyback offers to cushion the falling share prices and simultaneously consolidate their holdings.

A share buyback offer usually signals promoters’ belief that the prevailing value of the stock has gone lower than its fair value. When a cash-rich company goes for share buyback, it, inter alia, helps improve earnings per share, prevents potential hostile takeover and returns surplus cash to shareholders.

Recently announced Buybacks (From March 2020 till April 15, 2020)

Currently amid the COVID pandemic, when the stock prices have taken a southward trend, companies with cash surpluses are coming out with share buyback offers to repose confidence in the business and alleviate shareholder concerns. Some of the companies that came out with the buyback offers till April 15th are as under:

| Sl. No. | Name of Company | Buyback size (in Rs. Cr. |

| 1 | Emami Ltd | 200 |

| 2 | Motilal Oswal Financial Services Ltd | 150 |

| 3 | Ramkrishna Forgings Ltd | 40 |

| 4 | Dalmia Bharat Ltd | 500 |

| 5 | Sun Pharmaceutical Industries Ltd | 1700 |

| 6 | Sterlite Technologies Ltd | 145 |

| 7 | Delta Corp Ltd | 125 |

| 8 | Polyplex Corporation Ltd | 55 |

| 9 | Onmobile Global Ltd | 54 |

Already, in this 1.5 to 2-month time, the markets have seen almost 9 buyback offers, while in the last entire fiscal year, there were only 55 buyback offers.

Applicable Laws in a Share Buyback by listed entities:

- SEBI (Buyback of Securities) Regulations, 2018

- SEBI (SAST) Regulations, 2011;

- SEBI (LODR) Regulations, 2015;

- SEBI (PIT) Regulations, 2015;

- SEBI circular bearing reference number CIR/CFD/POLICYCELL/1/2015 dated April 13, 2015 read with the circular bearing reference number CFD/DCR2/CIR/P/2016/131 dated December 9, 2016

- Companies Act, 2013;

Whenever a company proposes a buyback, there always remain questions in the minds of Board of Directors/ Compliance Officers, as to various legal implications. Herein, we have attempted to compile a few of them, with their answers, in a simplified way.

SOME FREQUENTLY ASK QUESTIONS (FAQs) ON

BUYBACK OF EQUITY SHARES

1. What is Buyback?

A buyback, also known as a share repurchase, is when a company buys its own outstanding shares to reduce the number of shares available on the open market.

2. What are the most prevalent modes available for Buyback?

3. What type of companies should plan a Buyback?

Generally, following financial and capital position leads a company to decide a buyback of shares:

- Large capital base as compared to industry peers

- Rich cash reserves but no avenues/project to deploy that cash,

- Declining EPS of Company- the Company desirous of returning the excess cash to shareholders in order to improve the earning per share.

- Market Price of shares is too low & promoter holding is less and there is a scope to consolidate the same, to avoid the hostile takeover.

- Illiquid Company’s stock and shareholders are feeling stuck in the company, for instance, during the present COVID times.

4. Can Promoters can participate in a buyback offer?

Promoters can participate in a buyback offer, only when it is being done through tender offer.

5. Why companies go for Buyback?

| To improve EPS | To enhance consolidation of stake in the company. | To achieve optimum capital structure. |

| To improve Return on Capital, Return on net worth and to enhance the long-term shareholders value. | To prevent unwelcome takeover bids. | To support share price during periods of sluggish market conditions. |

| To provide an additional exit route to shareholders when shares are undervalued or are thinly traded. | To return surplus cash to shareholders. | To service the equity more efficiently. |

6. Is shareholders’ approval mandatory for a Buyback?

No. A Buyback can be undertaken even with a Board Resolution as well. However, the %age of buyback allowed is lesser therein.

7. What is the validity of the Shareholder Resolution/ Board Resolution?

The resolution for approval of buyback is valid for one year i.e. the buyback must be completed within 1 year from the date of Board Resolution or Shareholder Resolution as the case may be.

8. Can the shares under lock-in be bought back?

No, the shares which are under lock-in cannot be bought back until such restriction gets over.

9. What is the requirement w.r.t. Debt/Equity Ratio?

|

Post Buy-Back Debt-Equity Ratio shall not be less than |

||

| Secured + Unsecured-Debts | : | Paid-up capital + Free Reserves |

| 2 | : | 1 |

|

Note:

|

||

10. What is the maximum limit for buyback?

| Maximum Amount Available for Buyback | 25% or less of the aggregate paid up-capital and free reserves based on both standalone and consolidated financial statements of the company. |

| Maximum no. of equity shares that can be bought back | 25% of the paid-up equity share capital in that financial year. |

Note: if the buyback is from open market, then only 15% of total paid-up capital & Free Reserves can be utilized/available for the buyback.

11. Funds that can be utilized for buyback:

12. Is it mandatory to have any minimum time gap between 2 buyback offers?

Yes. The Company shall not make any offer of buy-back within a period of 1 year reckoned from the date of expiry of buyback period of the preceding offer of buy-back.

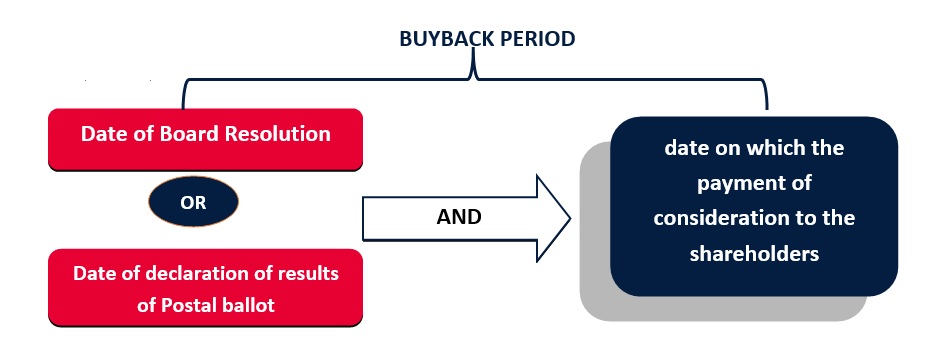

13. What is buyback Period?

Buyback Period means the period between:

14. Can a company withdraw the buyback offer, once announced?

No. A company cannot withdraw the offer to buy-back after the draft letter of offer is filed with SEBI or the Public Announcement of the offer to buy-back is made.

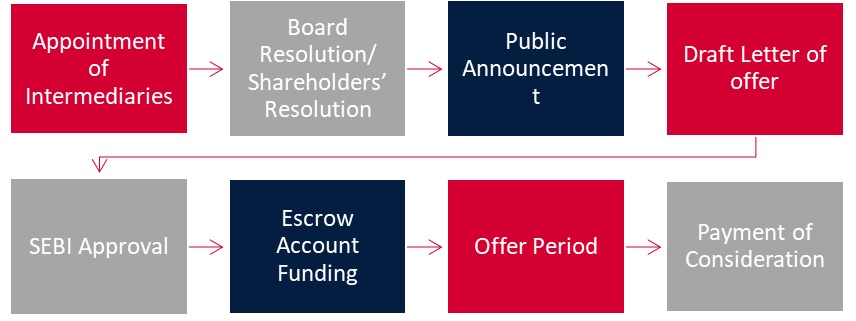

15. What are the major steps involved in a Buyback?

16. Can company issue new shares during /after the buyback period ?

- Issue of shares during the “Buyback Period”:

- Issue of shares post “Buyback Period”:

- Special relaxation to companies due to pandemic:

The company cannot issue any shares or other specified securities including by way of bonus, till the expiry of the buyback period for the offer. However, the company may issue the Grant Letters/ RSU Letter under an ongoing ESOP Scheme during the buyback period.

The Company cannot raise further capital for a period of 1 year from the expiry of buyback period, except in discharge of its subsisting obligations. That is, after the buyback period, the Company can issue shares only for discharging its subsisting obligations which includes issue of shares pursuant to conversion of warrants, stock option schemes, sweat equity or conversion of preference shares or conversion of debentures into equity shares.

SEBI, vide it’s circular dated 23rd April, 2020 curtailed the restriction on fresh fund raising by companies, after the buyback, to 6 months from 1 year earlier, in light of the coronavirus pandemic. This relaxation will be applicable till December 31, 2020.

17. Can a company make a Public Announcement for Buyback during the pendency of any scheme of amalgamation?

No, a company cannot make the public announcement of buy-back during the pendency of any scheme of amalgamation or compromise or arrangement pursuant to the provisions of the Companies Act.

18. Escrow Account obligations and mode of funding the Escrow A/c

Under the SEBI Buyback Regulations, in case of buyback of shares, an Escrow A/c is needed to be opened. The amount to be put in the Escrow A/c, the mode of funding, its utilisation etc depend upon the mode of Buyback chosen.

19. Can cash component of the escrow account in the buyback offer process be maintained in an interest-bearing account?

Yes, the cash component of the escrow account may be maintained in an interest-bearing account. However, the merchant banker is needed to ensure that the funds are available at the time of making payments to the shareholders.

20. What will be the impact of tax on buyback?

Under Section 115 QA of income Tax Act 1961, 20% Buyback Tax was introduced even for listed companies, in the Union budget 2019, w.e.f. July 5, 2019. According to this section, 20% tax (plus applicable surcharge & cess) will be levied on the difference between the issue price and the buyback price of the shares. The company shall be is liable to pay the same.

To exemplify, If XYZ Ltd originally issued shares for Rs 10/-. The shareholder bought the shares at Rs 400/-. The company goes in for buy-back of shares @ Rs 600/-. In such case, as per Section 115QA, tax is payable on Rs 590/- (Rs 600 –Rs 10) plus surcharge & cess, as applicable.

21. What if, post buyback, the holding of any shareholder breaches the threshold as prescribed under regulation 3 (1) & (2) of the SEBI (SAST) Regulation 2011. Will it trigger open offer?

An increase in voting rights of any shareholder beyond the limits attracting an obligation to make an open offer under regulation 3(1)/ (2) of SAST Regulations, pursuant to buy-back of shares by the target company, are exempt under Regulation 10, from the obligation to make an open offer provided such shareholder reduces his shareholding within 90 days from the date of the closure of the said buy-back offer and subject to other compliances as prescribed.

Hope you will find these useful, in planning your Corporate Actions. For any discussion, please feel free to contact us:

Anjali Aggarwal

Partner & Head – Capital Market Services

Corporate Professionals

anjali@indiacp.com

M: +91 9971673336

*****

Disclaimer: These FAQs have been prepared by Corporate Professionals on the basis of the various queries received from clients and others. It is meant to be merely an informative summary and should not be treated as our recommendation/ opinion and cannot be a substitute for considered legal advice.