The Registrar of Companies has been in the news these days for the slew of adjudication orders being passed under the various provisions of the Companies Act, 2013 (“the Act”), and more particularly related to Significant Beneficial Ownership (“SBO”). One such recent order involves LinkedIn Technology Information Pvt Ltd (“LinkedIn India”), whereby the Registrar of Companies, NCT of Delhi & Haryana (“RoC”) has levied penalties on LinkedIn India, its directors, and, more importantly, on Mr. Satya Nadella, CEO of Microsoft Corporation, and Mr. Ryan Roslansky, Global CEO of LinkedIn division within Microsoft Corporation. In this piece, we discuss the said order and why we think the said order fails to meet the requirements of section 90 of the Act concerning SBO.

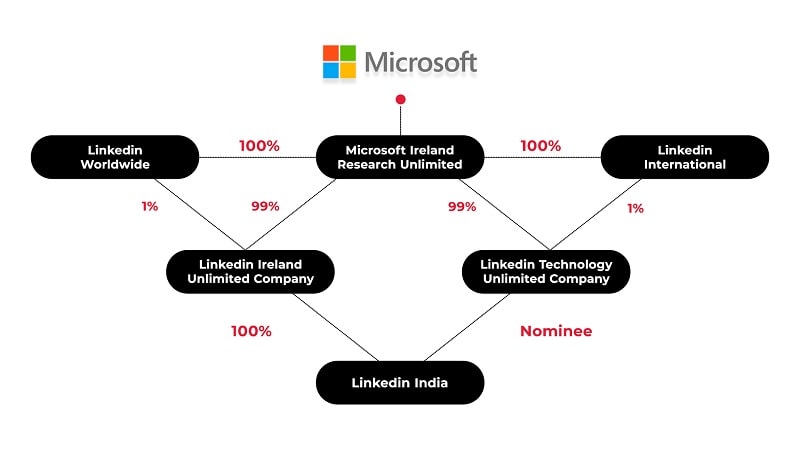

Current structure of LinkedIn India

The other material facts of the case as per the order are as follows:

- Mr. Satya Nadella is the Chairman & CEO of Microsoft Corporation whereas Mr. Roslansky serves as the Global CEO of LinkedIn division.

- Above Structure includes LinkedIn Corporation, USA, being owned and controlled by Microsoft Corporation, where Mr. Roslansky is an employee and the Global CEO.

- LinkedIn India has been showing LinkedIn Corporation, USA as its holding company in its financial statements filed with the RoC, while Microsoft Corporation is the ultimate parent company.

- Mr. Roslansky reports to Mr. Satya Nadella.

- As per LinkedIn India, at Microsoft Corporation., there is no individual shareholder who either owns the majority or exercises control or significant influence as per Section 90 of the Act.

- All the directors of LinkedIn India, whether in the past or present, are linked to and are employees of Microsoft Corporation.

- In certain board meetings of LinkedIn India, observers representing Microsoft Corporation remain present.

- Mr. Roslansky visited the LinkedIn India Office, where he met employees and Indian customers and simultaneously shared macro plans about Indian operations and the possible layoffs in India. Details of the said meeting including videos are available in the public domain.

- Bank accounts of LinkedIn India are operated by the employees of Microsoft Corporation duly authorized by the former’s Board of Directors.

RoC, has concluded that through various means and channels, Mr. Nadella and Mr. Roslansky are controlling LinkedIn India and are exercising significant influence over it, on the following grounds:

- Nominee/ Promoter Director Since employees of Microsoft Corp. and LinkedIn Corp. USA (‘Parent Companies’) have been designated as directors of LinkedIn India and such employees serve the interest of Parent Companies, thus they shall be considered as Nominee/ Promoter Directors. RoC also observed that these individuals hold multiple directorships in Microsoft and LinkedIn entities globally, suggesting a pattern of control.

- Leadership and Operational Control:

(a) Role of Mr. Roslansky: RoC has pointed out that Mr. Roslansky, the CEO of LinkedIn Corporation, has referred to LinkedIn as a group under his leadership, which includes LinkedIn India. This implies an overarching control and influence by Microsoft through LinkedIn Corporation over its subsidiaries, including LinkedIn India.(b) Day-to-Day Management: Although LinkedIn’s response asserts that Mr. Roslansky does not control day-to-day operations independently, RoC highlights that he exercises macro-level control, representing the group’s interests. R0C, while concluding the above, has rejected the contention of LinkedIn India that it is necessary to have a formal written arrangement to exercise control and significant influence.

- Delegation of Financial Powers:

Board Resolutions on Banking Operations: The ROC raised concerns about Board resolutions that delegate significant financial powers to the employees of Microsoft Corporation suggesting these individuals effectively control LinkedIn India’s financial operations. RoC has further argued that such delegations indicate a lack of independent financial control within LinkedIn India. - Governance Structure Post-Acquisition:

Integration into Microsoft’s Ecosystem: RoC has highlighted that post-acquisition, LinkedIn India has been integrated into Microsoft’s broader corporate structure, impacting its independent operational and financial decision-making processes. This integration is seen in the shared leadership and governance practices across Microsoft and LinkedIn entities. Moreover, the presence of observers, generally employees of Microsoft Corporation, in the board meetings of LinkedIn India, has added fuel to the said understanding.

Crux of RoC’s Contentions:

RoC’s allegations against LinkedIn India focuses on the extent of control exercised by Microsoft over LinkedIn, particularly through the appointment and control of directors, delegation of financial powers, and overall governance practices post-acquisition. Now, we analyze the above explanations provided by the ROC in the light of the provisions of SBO under the Act.

- General Corporate PracticesAt the onset and before dwelling on the provisions of the law, let’s try to understand how big corporates generally manage their group structure. In such groups, the companies within the group generally share resources and assets belonging to each other either with or without charges, and as regards to board structure, the parent company that is already in control of its subsidiaries designates/deputes their employees or employees of one group company as directors without any remuneration and without any change in employment where he/ she is actually employed. Depending upon the size of operations, board meetings of group companies or subsidiaries, generally have key personnel especially CFO, Legal Counsel, Company Secretary, etc., of the parent company present as invitees to provide inputs to the board about the plan or course of action of the group as a whole. Therefore, a parent company generally designates its key personnel such as CFO or CEO as Group CFO or Group CEO. These practices are generally adopted by corporates to create synergies amongst the group.

- Nominee DirectorThe concept of Nominee director as mentioned in section 161 of the Act, has been envisaged to take care of the interest of strategic or minority investors, debenture holders/ Lenders, etc. In other words, it means a nominee is generally appointed on the board on behalf of a person who is in the minority and not in control or lacks significant influence, which can’t be a parent company or promoter who otherwise has control either directly through shareholding or through subsidiaries in a group structure. Thus, employees so appointed by a parent company in its subsidiary cannot be considered as nominee directors but can be categorized as non-independent. This practice is recognized in section 167(1)(h) of the Act, where a director automatically ceases his office, who has been appointed by virtue of being in the employment of holding, subsidiary, or associate company, pursuant to the cessation of employment in that other company. Moreover, section 203 of the Act allows a whole-time Key Managerial Personnel of the parent company to hold office as such in any of its subsidiaries or hold a directorship in any other company even outside the group.

From the foregoing discussion, it can be said that the legislator has honored the aforementioned practices of corporate houses by recognizing the same in the Act and such practices cannot be covered under the definition of control and significant influence.

- Attendance of non-directors in a board meeting As we discussed, it is a normal practice amongst corporates to invite key personnel of the parent company to a board meeting or any other committee meeting, and at the same time, it is a prerogative of the board of directors to allow or not to allow any person other than director to attend the meeting. Even if an invitee or observer is not related to the parent company, then also, such person (or other than the person who he is representing) can’t be considered to exercise control or significant influence since such invitee or observer does not have any right to participate in a board meeting.

- Authorization to run bank accounts Under the Act, there is no restriction to authorize employees of the parent company to operate bank accounts of subsidiaries provided such authorization is backed by the board resolution of the latter. It means the ultimate authority to operate bank accounts is with the board and its continuity is subject to supervision of the board unless such authorization is rescinded by it subsequently.

Further, operating the bank accounts of a company falls under administrative acts of a routine nature when so authorized by the Board or to draw and endorse any cheque on the account of the company in any bank. Consequently, such acts cannot be categorized in any way as a mode of exercising ‘control’ or ‘significant influence’ in the company.

- CEOs’ Roles in Question While concluding that the CEO of LinkedIn Corp., USA (i.e., Mr. Roslansky) is exercising control and significant influence over LinkedIn India, RoC has considered the fact that the majority of directors of LinkedIn India are also directors or holding key positions at LinkedIn Corp., which means they are subordinates to Mr. Roslansky. Further, RoC also noted the fact that during his visit to India, he informed his plans about Indian operations, possible layoffs, and had meetings with employees and customers of the Indian subsidiary, etc., which tantamount to indirectly giving direction to the board of directors of LinkedIn India. Lastly, since Mr. Roslansky, in turn, reports to Mr. Nadella, who is the Chairman and CEO of Microsoft Corporation, as a result, Mr. Nadella also exercises control and significant influence over LinkedIn India through Mr. Roslansky.In our view, CEO per se has wide powers to manage the affairs of the company and the group. Accordingly, a CEO with materially vested powers will always have some sort of ‘control’ and ‘significant influence’ over the group, but that can’t be a sufficient reason to treat him as an SBO. If we look at the definition of ‘Managing Director’ and ‘Manager’ as provided under the Act, the board of directors of a company is required to vest them with the power and control to manage the affairs of the company but subject to supervision of the board otherwise such person occupying that office cannot be considered as such as he/ she is toothless to run the business of the company. In other words, it can be said that the office of a CEO, which may be vested with control and significant influence is always subject to supervision of the board of directors, which means once that CEO ceases his/ her office, then the control and significant he/ she was exercising would also come to an end. Whereas under SBO Law, the objective is to identify an individual as an SBO who exercises autonomous and absolute control or significant influence without any restriction, and which is not attached to any office. That SBO so identified shall remain in control till such time as he/ she wishes and not at the will of other persons. That’s why in the definition of ‘Promoter’, proviso exempts a person who acts in the capacity of a professional from being termed as a promoter who is in control over the affairs of the company.

Conclusion

LinkedIn India has demonstrated that its governance and operational practices are in line with standard corporate norms and legal provisions. The presence of Microsoft’s personnel on LinkedIn India’s governance structure is intended to ensure strategic alignment and does not equate to undue control or influence. LinkedIn India continues to operate with a degree of independence appropriate for a subsidiary within a larger corporate group, maintaining compliance with all relevant regulations and laws. The order in the LinkedIn matter seems to undermine the objective behind the provisions of SBO i.e., to unearth the real promoter who is in control behind a complex corporate structure. In the foregoing matter, it is a well-known fact that Microsoft Corporation is the ultimate parent company of LinkedIn India, with Mr. Nadella as its CEO. Thus, categorizing Mr. Nadella as an SBO is not in line with the intent of SBO Law and is a fit case to be challenged before the Regional Director, Ministry of Corporate Affairs or Hon’ble High Court in the form of a writ.

Till the said order is challenged before the appellate authority, the RoC’s interpretation and actions against LinkedIn India and Microsoft could set a precedent with far-reaching consequences for other corporates, including Indian corporate houses, who also adopt such practices and a similar governance structure. While aimed at ensuring compliance and transparency, such stringent interpretations could inadvertently stifle operational efficiency, strategic alignment, and foreign investment.