With total of 16 unicorns (start-up with a valuation of over $1 billion) and more than $11 billion in funding, mainly from the US-based investment firms (till June – end) as mentioned below in 2021 alone.

|

Indian Startup Unicorns in 2021 |

|||

|

Sr. No. |

Unicorn Name |

Valuation (in $ billion) |

Sector |

|

1 |

Digit Insurance |

1.9 |

Insurance |

|

2 |

Innovaccer |

1.3 |

Software |

|

3 |

Infra.Market |

1 |

Infrastructure |

|

4 |

Five Star Business Finance |

1.4 |

Banking |

|

5 |

Meesho |

2.1 |

Social Commerce |

|

6 |

Cred |

2.2 |

Fintech |

|

7 |

Pharmeasy |

1.5 |

E-Pharmacy |

|

8 |

Groww |

1.0 |

Stockbroking |

|

9 |

Mohalla Tech (Sharechat and Moj) |

2.1 |

Social Media |

|

10 |

Gupshup |

1.4 |

Enterprise Messaging |

|

11 |

Chargebee |

1.4 |

Fintech |

|

12 |

Urban Company |

2.0 |

Home Service |

|

13 |

Moglix |

1.0 |

B2B E-commerce |

|

14 |

Zeta |

1.5 |

Banking Technology |

|

15 |

Browserstack |

4.0 |

SaaS |

|

16 |

BlackBuck |

1.0 |

Logistics |

In this complex financial and economic world, valuing all sorts of companies has become necessary for a number of reasons, be it Investment, Acquisition, Merger or even a statutory purpose. At the same time the difficulty for the valuers has also increased due to such dynamic environment. Therefore, it would be difficult to value all the companies using the same methodologies.

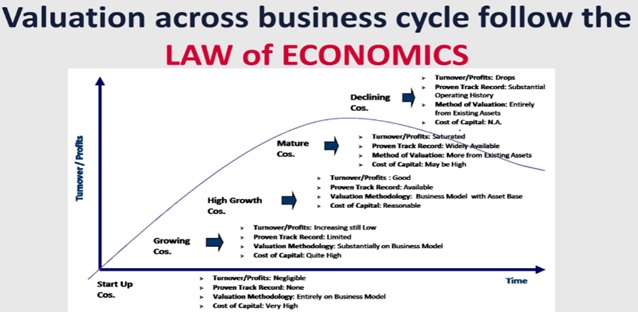

Businesses at different stages of their life-cycle demand different methodologies for their valuations. The below chart shows, how the life cycle of a business affects the valuation approach:

Focusing on the start-up companies or early stage companies, we can say that Start-up valuation is more about understanding promoter’s and management background, experience and vision, future potential of business, people, technology, competitive landscape, traction and the probability of success and failure attached with the start-up. In a way, Start-up valuation also involves validation/review of business model which makes it complicated vis-à-vis other valuations. It can be concluded that while valuating a Start-up, the experience of valuer plays a significant role in value conclusion as its certainly is an art, not the science.

- No history, operations has not reached commercial production

- Negligible revenues with high operational losses / Negative Cash Flows

- Limited capital infused by promoter and high dependence on external source of funds

- Illiquid Investments

- Speculative/Aggressive Financial Projections

- High Risk Companies

- Complex Capital Structure

In the recent times, many technology and e-commerce (B2C) companies were distinguished. Most of these companies created decent sales but could not create profits due to lack of sustainable business model.

Most of the valuers have hard time valuing Start-ups because of the great uncertainty surrounding potential market size, profitability and required investments. Financial multiples that normally provide a benchmark for valuation are rendered futile because profitability is often negative.

Whenever investors are ready to infuse money, academics and practitioners rely on non-financial multiples, which compare enterprise value with one or more non-operating metrics, such as web site hits, unique visitors, number of subscribers or gross merchandising value (GMV) etc.

However, it is strongly emphasised that the non-financial metrics must be a reasonable predicator of future value creation, and thus somehow tied to ROCE and growth. Non-financial multiples should be used only when they can be connected to the financial multiples. For example, if a company cannot translate visitors, page views, subscribers or GMV into profits and cash flows or the same cannot be validated on the valuation date, the non-financial metric turn illogical, and use of such multiples should be avoided.

In such a case, it then remains as an investor’s call on the founders and transactions takes place at the price equilibrium considering the demand-supply characteristics.

Whatever multiple selected for valuing the company, the following methods should be applied on such valuation to account for such risky venture.

For valuing companies there are three approaches i.e. Asset, Income and Market approach; however, for Early stage companies “Market Approach” is recommended, as the long-term projections are speculative/aggressive at this stage.

-

- Where independent investment has not yet been made in the company:

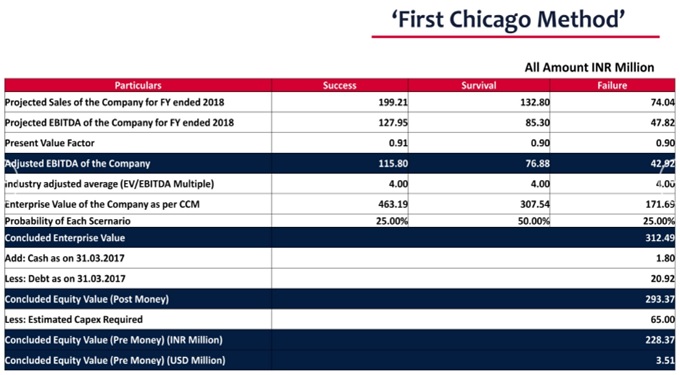

- First Chicago MethodThe First Chicago method entails three different projections – Success, Failure and Survival cases – and profitability estimates a assigned to each case.

This method eventually results in a separate valuation and pricing for each outcome. These heads are then averaged and the weighted average valuation is determined (weights being the probability assigned to each case).

- First Chicago MethodThe First Chicago method entails three different projections – Success, Failure and Survival cases – and profitability estimates a assigned to each case.

- Where independent investment has not yet been made in the company:

-

-

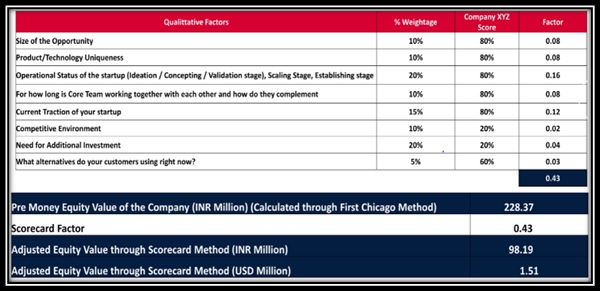

- Scorecard MethodThe Scorecard valuation method is a more elaborated approach to the subject company valuation. It starts in the same way as the First Chicago Method i.e. you determine a base valuation for a certain set of criteria except, those criteria are themselves weighted up based on their impact on the overall success of the subject company. Besides the normal valuation of a company the scorecard method considers the qualitative scores of management, traction, competition, etc. The weighted average value is recommended as the value through Score Card methodology.

-

-

- Exit Multiple MethodAs Start-ups are high risk companies, investors expect higher returns. The Exit Multiple method takes into account the current investment, the expected return, and the valuation at the time of exit to determine the current value of the company by discounting it back by the expected return.

- Where independent investment has been made in the company:

- Reverse Calculation or Back Solve MethodThis method derives the implied equity value for the Company from a transaction involving the company’s own securities, typically, the preferred stock.

It indicates an equity value that is consistent with the rate of return that investors in the most recent round expected given the degree of marketability of their investment as well as any special rights (e.g. liquidation preferences) accorded to them.

- Reverse Calculation or Back Solve MethodThis method derives the implied equity value for the Company from a transaction involving the company’s own securities, typically, the preferred stock.

Traditionally, valuations of companies were based on historical financials like EBITDA, revenue, Profit after Tax etc. However, valuations of the start-ups are currently being performed by various other factors like their impact in the market, number of subscribers, database which they have, eventually which will lead to future revenue for the companies. These will lead loss making companies with higher valuations in their initial years.

Selection of Valuation methodology for start-up are based on the company’s life cycle, characteristics and experience of valuer.