1. From which date will the amended provisions of the Stamp Act and Rules made thereunder come into force?

Answer

The amended provisions of the Indian Stamp Act, 1899 brought through Finance Act, 2019 and the Rules made thereunder have come into force w.e.f 1st July, 2020.

2. Which securities are covered under the Stamp Act post amendment?

Answer:

Securities covered would include

(a) “securities” as defined under section 2(h) of Securities Contracts (Regulation) Act, 1956; (shares, debentures, derivatives, units of mutual funds, Government Securities, etc.)

(b) “derivative” as defined in clause (a) of Section 45U of the Reserve Bank of India Act, 1934;

(c) a certificate of deposit, commercial usance bill, commercial paper and such other debt instrument of original or initial maturity up to one year as the Reserve Bank of India may specify from time to time;

(d) repo on corporate bonds; and

(c) any other instrument declared by the Central Government, by notification in the Official Gazette, to be securities for the purposes of this Act.

3. Under the new framework, what shall be the instruments on which stamp duty shall be levied in connection with issuance or transfer of securities?

Answer: Under the new framework, stamp duty will be levied on the following instruments depending upon the nature of the transactions:

| S.No. | Nature of Transaction | Name of the Instrument |

| I. | Sale of securities through stock exchange | Clearance List |

| II. | Sale of securities through Depository incl. off market transfers, over the counter, etc other than through stock exchanges | delivery instruction Slip |

| III. | Issue of securities in demat mode | Allotment List |

| IV. | Sale of securities through physical mode | Transfer deed |

| V. | Issue of securities in physical form in case of private limited company | No instrument is mentioned |

4. Who is liable to pay stamp duty?

Answer: Under the earlier framework, there was no clarity on the responsibility of payment of stamp duty. The stamp duty was paid either by the buyer or the seller as agreed between the parties to the transaction. However, under the new framework, the responsibility to pay stamp duty is fixed on the basis of the nature of transaction: –

| S.No. | Nature of Transaction | Responsibility |

| I. | In case of transfer through stock exchange | Buyer |

| II. | In case of transfer through depositories otherwise than through stock exchange | Seller |

| III. | In case of transfer of securities in physical form | Seller |

| IV. | In case of issuance of securities, in dematerialized mode or physical form | Company/Issuer |

| V. | In case of tender offer (buyback, delisting), open offer, offer for sale (right issue, IPO) or private placement through stock exchange | buyer once the offer is successfully completed |

5. When will the stamp duty be collected under the new framework?

Answer: The stamp duty shall be collected as follows:-

| S.No. | Nature of Transaction | Time/ day |

| I. | Sale of securities through stock exchange | On the settlement day |

| II. | Sale of securities through Depository incl. off market transfers, over the counter, etc other than through stock exchanges | Before execution of transaction |

| III. | Issue of securities in demat mode | Before making changes in the records of Depository |

| IV. | Sale of securities through physical mode | At the time of executing Transfer deed |

| V. | Issue of securities in physical form in case of private limited company | Within 30 days of the issuance of shares |

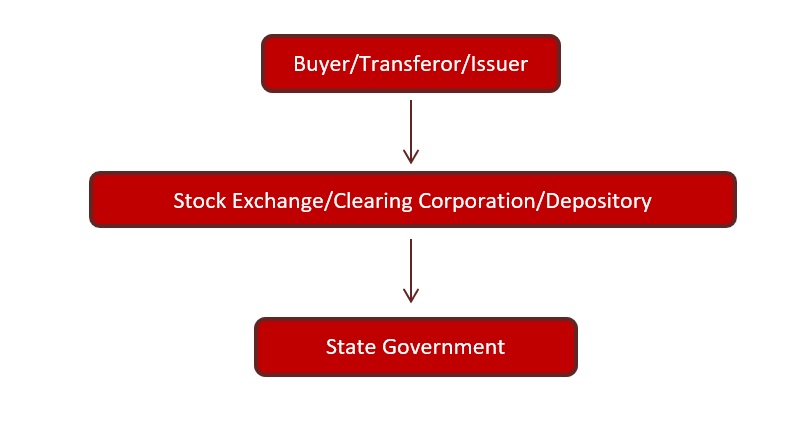

6. What is the procedure to pay stamp duty under the new framework?

Answer:

Step 1: The buyer or transferor or issuer, as the case may be, shall pay stamp duty to the Stock Exchange or Clearing Corporation or Depository, as the case may be.

Step 2: Thereafter, the Stock Exchange/Clearing Corporation/Depository shall transfer the collected stamp duty within 3 weeks of the end of each month after deducting facilitation charges to the State Government where the residence of the buyer is located and in case the buyer is located outside India, to the State Government having the registered office of the trading member or broker of such buyer and in case where there is no such trading member of the buyer, to the State Government having the registered office of the participant.

Step 3: The Collecting Agent shall then transfer the collected stamp-duty in the account of concerned State Government with the Reserve Bank of India or any scheduled commercial bank, as informed to the Collecting Agent by the Reserve Bank of India or the concerned State Government.

7. What is the collection and deposit of stamp duty mechanism under the new framework?

Answer: The collection and deposit mechanism of stamp duty under the new framework are as follows:

(a) Transfer of securities through stock exchange– the buyer will pay the stamp duty to the Stock Exchange or Clearing Corporation who will further deposit the same to the respective State Governments where residence of buyer is located.

(b) Transfer of securities through depository– the seller will pay the stamp duty to the Depository who will further deposit the same to the respective State Governments where residence of buyer is located.

(c) Issue of securities through demat mode – the issuer/company will pay the stamp duty to the Depository who will further deposit the same to the respective State Governments where residence of buyer is located.

(d) Issue of securities other than through stock exchange or through depository– The issuer/company will pay the stamp duty directly to the State Government where the registered office of the Company/ Issuer is situated.

(e) Transfer of securities other than through stock exchange or demat mode- The Central Government is only eligible to levy and collect stamp duty.

8. Who is eligible to collect stamp duty?

Answer: The followings are eligible to collect stamp duty under the new framework:-

(a) Stock Exchanges

(b) Clearing Corporation of India Limited (CCIL)

(c) Depositories- NSDL and CDSL

(d) Registrars to Issue and / or Share Transfer Agents

The aforementioned entities are collectively recognized as ‘collecting agents’ under the new framework.

9. Which State Government is eligible to receive stamp duty from collecting agents?

Answer: The right to levy stamp duty is a state subject under the Constitution of India. The eligibility of the respective State Governments to receive stamp duty will be determined on the basis of the State where the buyer resides to be called as ‘Domicile State’. Here, the permanent address (or in absence thereof, the correspondence address) of the buyer shall be the Domicile State as per the records of the stock exchange, clearing corporation or depository.

10. Which State Government is eligible to receive stamp duty in case of issue of securities by listed/ unlisted public company and issue of securities by private company?

Answer:

i. In case of issue of securities by a listed/ unlisted public company, multiple State Governments may be eligible to receive stamp duty depending the criteria of Domicile State of the buyers.

ii. In case of issue of securities by a private company, only one (1) state government is eligible to receive stamp duty where the registered office of the issuer/ company is situated.

11. If shares are issued/allotted on 1st September, 2019 but share certificates are executed on or after July 1, 2020. Then, under which framework – new or old will the stamp duty be levied?

Answer: The new framework which became effective from July 1, 2020 talks of only issuance of securities to levy the stamp duty. In case the issuance of securities is preceding the effective date of new framework, the stamp duty on such issuance will be levied as per the old regime.

12.What shall be the basis of calculation of stamp duty?

Answer: The stamp duty shall be calculated on the basis of market value of securities which are subject to issuance or transfer, as the case may be.

13. What is the meaning of the term ‘market value’ under the new framework?

Answer: The Market Value is the consideration involved in any transaction and will be determined in following manner –

| S.No. | Nature of Transaction | Market Value |

| I. | Sale of securities through Stock Exchange | Traded Price |

| II. | Sale of securities through Depository incl. off market transfers, over the counter, etc other than through stock exchanges | Consideration/ price mentioned in delivery instruction Slip |

| III. | Issue of securities in demat mode | Issue Price mentioned in Allotment List |

| IV. | Sale of securities through physical mode | Consideration as mentioned in Transfer Deed |

| V. | Issue of securities in physical form in case of private limited company | Consideration/ Issue Price |

14. What are the revised rates of stamp duty?

Answer: The key rates of stamp duty under the new framework are as follows:-

| S.No. | Instrument | Rate of Stamp Duty Post Amendment |

| 1. | Issue of Debentures | 0.005% |

| 2. | Transfer and Re-Issue of debentures | 0.0001% |

| 3. | Issue of security other than debentures | 0.005% |

| 4. | Transfer of security other than debenture on delivery basis | 0.015% |

| 5. | Transfer of security other than debenture on non-delivery basis | 0.003% |

| 6. | Derivatives | |

| Futures (equity and commodity) | 0.002% | |

| Options (equity and commodity) | 0.003% | |

| Currency and interest rate derivatives | 0.0001% | |

| Other derivatives | 0.002% | |

| 7. | Government securities | 0% |

| 8. | Repo on corporate bonds | 0.00001% |

15. In case of allotment of shares in private company, when the stamp duty will be levied – whether on allotment of shares or issuance of share certificates?

Answer: The stamp duty shall be levied on the allotment of shares irrespective of the fact that the share certificates pursuant to such allotment are issued or not.

16. Whether stamp duty will be levied on conversion of debentures or preference shares into equity shares where stamp duty has already been paid on such debentures or preference shares?

Answer: If there is consideration involved at the time of conversion of debentures or preference shares into equity shares, the stamp duty will be levied on issuance of equity shares. However, if there is no consideration involved at the time of conversion, no stamp duty will be levied.

17. Whether stamp duty will be levied in case of conversion of loan into equity shares?

Answer: Under the Companies Act, 2013, allotment of shares against conversion of loan is not considered as ‘issue of shares for consideration other than cash’. Thus, whatever be the outstanding loan to be converted into shares will be subject to stamp duty.

18. Whether stamp duty will be levied on transfer of shares through demat mode?

Answer: Under old regime, the transfer of shares through demat mode did not attract stamp duty whereas under new regime, transfer of shares in any mode incl. demat mode is liable to stamp duty.

19. Whether stamp duty will be levied on Bonus Shares?

Answer: As per the new framework, the stamp duty is to be collected on market value which comprises of only price or consideration involved in the transaction. In case of issuance of bonus shares, no consideration/ price is involved and thus, no stamp duty will be levied.

20. How will the stamp duty be levied on transfer of shares in physical form in case of a private company?

Answer: Under the new framework, there is no explicit right vested with the State Government to levy and receive stamp duty on transfer of securities in physical mode unlike in case of transfer through stock exchange or depository. Thus, the Union Government shall continue to collect the stamp duty on transfer of shares in physical form as per the revised rates. Further, in terms of the Constitution of India, the power to levy and collect the stamp duty on transfer of shares vests with the Union Government.

21. What is the price to be taken on which stamp duty will be calculated in case of ESOP and Sweat Equity?

Answer: Under the new framework, the stamp duty shall be calculated based on the consideration involved in the issuance of ESOP or Sweat Equity Shares irrespective of the market price on the stock exchange or valuation carried out by the Company.

22. Is gift of securities liable to stamp duty under the new framework? What will be value at which stamp duty shall be levied in such cases?

Answer: The stamp duty is to be collected on market value based on price or consideration involved. Accordingly, since consideration involved in case of gift is “Nil”, no stamp duty will be levied in such transaction.

23. Whether stamp duty shall be levied on invocation of pledge? If yes, how will it be paid and on what value stamp duty will be levied?

Answer: The invocation of pledge shall attract stamp duty under the new framework. Here, the stamp duty shall be paid by the pledgee (Banks or Financial institutions) on the consideration amount mentioned in the agreement of pledge.

24. How stamp duty shall be levied in the following cases of transfer:-

A. Transfer of shares by Non-Resident to Indian resident

Answer:

The due stamp duty shall be levied once the share transfer form (SH-4) is executed by the two parties.

B. Transfer of shares by one Non-Resident to another Non-Resident

Answer:

In case the share transfer form/ instrument is executed outside India, the stamp duty shall be payable within 3 months from the date it is received in India. (refer section 32 of Indian Stamp Act, 1899)

25. Which transactions are not subject to stamp duty by Depository?

Answer: Following cases where there is no change in beneficial ownership on account of creation or destruction of securities due to corporate actions such as

(a) Stock split;

(b) Stock consolidation;

(c) Buyback; and

(d) Merger and acquisitions (like cancellation of cross investments/ shareholdings)

shall not be subject to stamp duty.

Here, it is pertinent to note that if there is a fresh issue to an investor as part of a corporate action, such issue shall be subject to stamp duty.

26. Whether stamp duty shall be levied on transfer of securities on account of operation of law such as succession, inheritance etc.?

Answer: The amended Indian stamp Act clearly indicates that stamp duty shall be collected on the basis of market value which is based on the price or consideration involved. In the absence of any consideration in transfer of securities pursuant to operation of law such as transmission of securities, succession /inheritance cases, no stamp duty shall be levied.

27. Who will collect and transfer the Stamp Duty to States in case of following transactions relating to Mutual Funds:

A. Transactions in units of Mutual Funds in Statement of Account/ Physical (non- demat/ physical form)

Answer: To provide for collection of Stamp Duty on transactions in mutual fund units in the statement of account/physical (non-demat) form, RTI and/or STA have been notified as a “Depository” for the limited purposes of acting as a “collecting agent”. Accordingly, for non-demat mutual fund transactions, collection of stamp duty shall be done by RTAs on behalf of the State Government and the transfer of stamp duty to the respective States based on residence of the buyer and not on the basis of registered office of the issuer.

B. Transactions in units of Mutual Funds (sale, transfer and issue of units in demat form) through recognized stock exchange or depository

Answer: In case of mutual fund transactions (sale, transfer and issue of units in demat mode) through recognized Stock Exchange or Depository as defined under SCRA, 1956 and Depositories Act, 1996 respectively, the respective Stock Exchange/authorized Clearing Corporation or a Depository is empowered to collect stamp duty as per the amended Indian Stamp Act and Rules made thereunder.

28. What will be the process of collection and remittance of stamp duty in case of transfer of mutual fund units held in physical form?

Answer: Where Mutual Fund units are issued in physical form, stamp duty has to be collected and remitted by RTA. Accordingly, when the transferee approaches RTA for effecting the transfer in their books, the RTA will be collecting the stamp duty from the transferor before effecting the transfer which will then be remitted to the State of domicile of the transferee.

29. On what value will the stamp duty be levied in case of issuance of mutual fund units?

Answer: Stamp duty is imposed on the value of units excluding other charges like service charge, AMC fee, GST etc.

30. Whether the following will attract stamp duty:-

A. Switching in mutual fund

Answer: The issue of fresh units in the switched scheme would also attract stamp duty even though there is no physical consideration paid or transfer of ownership. This is because the new units are deemed to have been purchased with the NAV realized from the sale of earlier units.

B. Redemption of mutual fund units

Answer: Redemption is not liable to duty as it is neither a transfer nor an issue nor a sale.