Jan 21, 2025

Things to Keep in Mind While Doing ESOP Valuation (Valuer’s Perspective)

Employee Stock Option Plans (ESOPs) are a popular way to reward and incentivize employees in India, especially among startups. Valuing ESOPs from an accounting perspective is a critical task, as it involves determining the fair value of options granted to employees and accounting for them in the company’s financials. Below is a detailed guide, along with examples, to help clarify key considerations when performing ESOP accounting valuations in India.

1. Which Legal Framework require ESOP Valuation in India?

ESOPs in India are governed by the Companies Act, 2013 and the Securities and Exchange Board of India (SEBI) regulations. For listed companies, SEBI (Share Based Employee Benefits) Regulations, 2014 apply. For unlisted companies, specific provisions under the Companies Act apply. It’s essential to comply with these legal frameworks to avoid regulatory issues.

Example:

If a listed company issues ESOPs to its employees, it must follow SEBI guidelines, which include detailed disclosure requirements. An unlisted company will need to ensure compliance with the Companies Act, including approval of the ESOP plan by a shareholders’ resolution.

2. Accounting Standards: Ind AS 102

In India, ESOP accounting must follow Ind AS 102: Share-Based Payments. This standard requires companies to recognize the cost of employee stock options at fair value, measured on the grant date, and expense this cost over the vesting period. The fair value is typically determined using an option-pricing model like Black-Scholes.

Example:

Consider a company granting 1,000 ESOPs to an employee with a vesting period of 3 years. If the fair value of each option at the grant date is ₹100, the total ESOP cost would be ₹1,00,000. The company would recognize an annual compensation cost of ₹33,333 (₹1,00,000 ÷ 3) over the three-year vesting period.

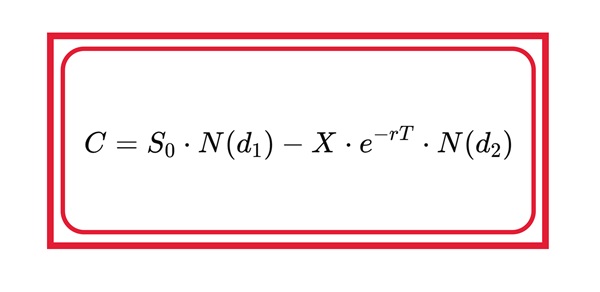

3. Valuation Method: Black-Scholes vs. Binomial Models

Black Scholes Method

The Black-Scholes Option Pricing Model is widely used for ESOP valuations in India due to its simplicity. It takes into account factors such as the stock price at grant, exercise price, time to maturity, volatility, risk-free interest rate, and dividends.

Where:

- C = fair value of the ESOP (or option price)

- S0 = current market price of the underlying stock (fair value of the company’s stock)

- X = exercise (strike) price of the option

- r = risk-free interest rate (e.g., yield on government bonds)

- T = vesting period or expected life of the option (in years)

- N(d1) and N(d2) = cumulative distribution functions for a standard normal distribution

- σ = volatility of the underlying stock

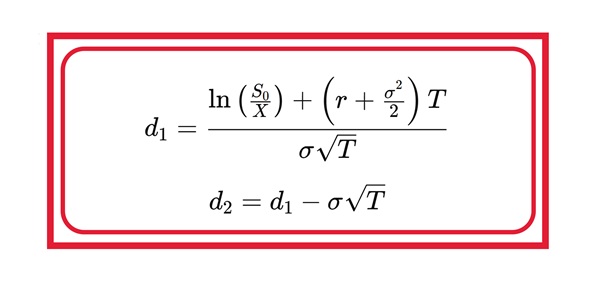

Calculation of d1 and d2:

Example:

A company grants options with an exercise price of ₹100, and the current market price of the stock is ₹120. Using Black-Scholes, the company’s expected volatility of 25%, risk-free interest rate of 7%, and option duration of 5 years would determine the fair value of these options. If Black-Scholes calculates a fair value of ₹30 per option, this amount must be recognized as employee compensation.

1. Fair Value vs. Intrinsic Value

Ind AS 102 requires companies to value ESOPs based on fair value, which is calculated using models like Black-Scholes or Binomial, as opposed to the simpler intrinsic value (the difference between the exercise price and the market price of the stock at the time of the grant).

Example:

If the exercise price of the option is ₹150, and the stock’s market price on the grant date is ₹160, the intrinsic value is ₹10. However, using the Black-Scholes model, considering volatility and time to maturity, the fair value could be ₹50. Under Ind AS 102, the company would account for the higher fair value, providing a more accurate reflection of the actual cost of the ESOP.

2. Volatility of the Stock

One of the key inputs in ESOP valuation is the stock’s volatility. For listed companies, historical stock price volatility can be easily calculated. However, for unlisted companies, it’s more challenging, and they typically estimate volatility using comparable listed companies from the same industry.

Example:

An unlisted fintech company offering ESOPs estimates its stock volatility at 30%, based on similar listed fintech firms. This estimated volatility directly impacts the option’s fair value—higher volatility generally increases the option’s fair value due to higher expected future gains.

3. Discount for Illiquidity

For unlisted companies, stock options may lack liquidity, as there is no public market for the shares. Therefore, a discount for lack of marketability (DLOM) is applied to account for this illiquidity, reducing the fair value of the ESOP.

Example:

An unlisted startup grants stock options to employees, but the shares are not publicly tradable. To reflect this illiquidity, the company applies a 20% DLOM. If the fair value of the option before DLOM is ₹100, applying the discount reduces the fair value to ₹80.

4. Vesting Conditions and Expected Life of Options

The vesting period and conditions attached to ESOPs affect their valuation. Most companies have time-based vesting, but some may have performance-based vesting, which needs to be factored into the valuation.

Example:

A company grants 1,000 stock options with a four-year vesting schedule. If the company’s valuation shows the fair value per option to be ₹50, the company will record an annual expense of ₹12,500 (1,000 options x ₹50 ÷ 4 years). If the options have performance conditions (e.g., revenue targets), this adds complexity and may require adjustments to the fair value.

5. Risk-Free Rate and Dividend Yield

The risk-free rate is usually based on government bonds of equivalent maturity to the ESOP term. If the company pays dividends, the expected dividend yield should also be included in the valuation model.

Example:

If a company uses the Black-Scholes model and the risk-free rate (based on 5-year Indian Government bonds) is 6.5%, it will input this figure into the model. If the company expects to pay a 2% dividend, this will also impact the fair value of the option, lowering it slightly since dividends reduce the stock’s appreciation potential.

6. Employee Turnover and Forfeiture Rate

It’s important to estimate how many employees will leave before their options vest. This forfeiture rate reduces the cost of ESOPs as forfeited options don’t result in compensation expense.

Example:

A company has a 10% annual employee turnover rate. If 1,000 options are granted, the company may estimate that 100 employees will leave before vesting, and thus only 900 options need to be accounted for in the ESOP valuation.

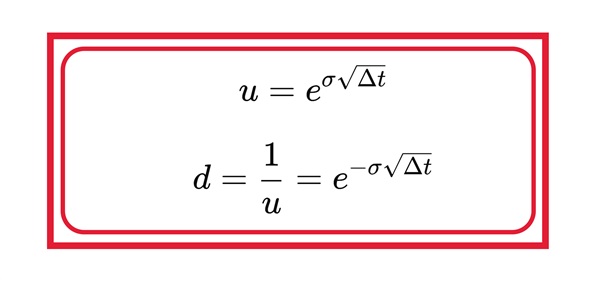

Binomial Method

The binomial method (also known as the binomial options pricing model) is a popular approach used for valuing employee stock options (ESOPs). It provides a way to model the possible future paths of an underlying stock price, taking into account the complexities of real-world market movements, such as early exercise by employees, vesting periods, and stock price volatility. The model involves constructing a binomial tree of possible stock prices over time, allowing for flexibility in handling American-style options, which can be exercised before expiration.

1. Set Up the Stock Price Tree:

- Create a tree structure that represents potential stock price movements over time. At each time step, the stock price can move up or down.

- The length of the option’s life is divided into equal time intervals.

The price at any point in the tree is calculated by either moving up by a factor uor down by a factor d:

Where:

- σ = volatility of the stock price

- Δt = length of each time step (total option life divided by the number of steps)

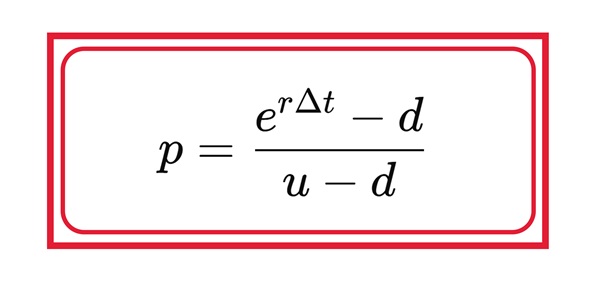

2. Calculate the Risk-Neutral Probabilities:

- The probability of an upward price movement in each time step is denoted by p, while the probability of a downward movement is 1− p.

The risk-neutral probability p is calculated as:

Where:

- r = risk-free rate (e.g., government bond yield)

- d = downward price factor

- u = upward price factor

3. Model Vesting Periods:

- ESOPs often come with vesting schedules (e.g., options vest after a few years). During the vesting period, employees typically cannot exercise the options. This needs to be factored into the model by ensuring no exercise happens before vesting is complete.

- If the employee leaves the company during the vesting period, the options may be forfeited, and this probability can be incorporated into the model.

4. Option Payoff at Maturity:

- At the end of the option’s life (at maturity), calculate the payoff at each final node in the tree, which will depend on whether the option is a call or a put:

- For a call option: Payoff = max (S−X,0)

- For a put option: Payoff = max (X−S,0)

Where:

- S = stock price at that node

- X = exercise (strike) price of the option

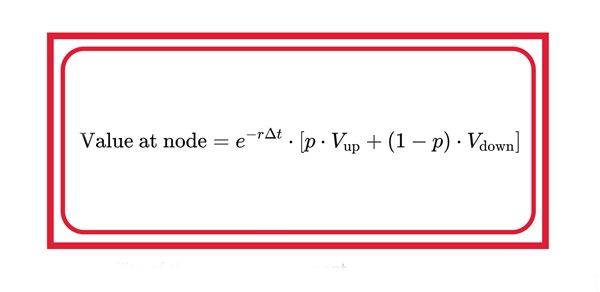

5. Backward Induction:

- Work backwards through the tree to calculate the option’s value at each earlier node. The value at each node is the discounted expected value from the next time step (i.e., a weighted average of the up and down future values).

Where:

- Vup = option value at the upward movement node

- Vdown = option value at the downward movement node

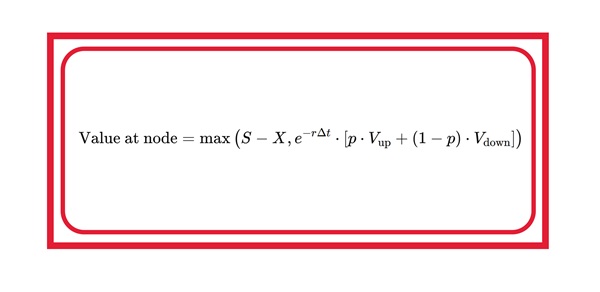

6. Early Exercise (Optional):

- If early exercise is allowed (common for ESOPs), compare the immediate exercise value with the value from holding the option. The option value at each node is the greater of:

- The intrinsic value (if exercised immediately)

- The expected value of holding the option

For a call option:

7. Incorporating Employee-Specific Features:

- Turnover/Forfeiture Rate: Since some employees may leave before their options vest, the probability of forfeiture can be included in the model to discount the option’s value accordingly.

- Expected Option Life: Employees often exercise their options earlier than the full vesting period. The expected life of the option, shorter than the contractual life, should be considered in the model.

4. Expense Recognition and Disclosure

Under Ind AS 102, companies must recognize the cost of ESOPs in their profit and loss statement over the vesting period. Additionally, transparent disclosures are required in financial statements, including the nature of the ESOP, how fair value was calculated, and the number of options outstanding.

Example:

If a company grants ESOPs valued at ₹1,00,000 over a 3-year vesting period, it must recognize ₹33,333 as an employee compensation expense each year. The financial statements should also disclose the methodology used for valuation and any changes in the number of ESOPs granted or forfeited.

Conclusion

A well-executed ESOP valuation in India not only ensures compliance with legal and accounting standards but also serves as a strategic tool to attract and retain top talent. Properly valued ESOPs align employee incentives with the company’s long-term goals, fostering a sense of ownership and commitment. By offering employees a share in future growth, companies can motivate them to perform better, boosting overall productivity. Additionally, transparent, and fair ESOP valuations enhance trust, reducing potential legal risks and financial discrepancies, thereby strengthening the company’s financial stability and market reputation.